As the U.S. stock market has, on average, outperformed international equities over the last 15 years since emerging from the Great Recession of 2008, many investors argue that international diversification is a poor allocation of dollars that would otherwise be earning more in the U.S. market. The outperformance of U.S. stocks has led to the favoritism of ‘local’ investments over international ones through behavioral biases (e.g., recency bias and the tendency to confuse the familiar with the safe) that have swayed investors (and some advisors) away from international diversification entirely. However, despite recent market trends, there is a legitimate case to be made for international diversification – starting with the basic tenet of investing that past performance does not promise future returns.

In this guest post, Larry Swedroe, head of financial and economic research at Buckingham Strategic Wealth, discusses why many investors tend to fall prey to recency bias, and explains why global diversification – and keeping short- and long-term results in the right perspective – remains a prudent strategy.

One common argument made by investors who refrain from global diversification is that, during systemic financial crises, everything does poorly, leading them to question the protection that international diversification offers during large market declines. While research may support this argument – that worst-case real returns for individual countries do tend to correspond with severe declines across all countries globally – the trend generally holds true only for the short term and the similarities in market behavior for countries around the globe tend to deteriorate over the long-term, as different countries naturally recover at different rates. But because no one can be sure of when and where these recoveries will happen, investors who are willing to spread the risk of slightly lower returns from globally diversified portfolios stand to yield the rewards of having an edge in the natural cycle of global markets in the aggregate.

Contrary to the view that global diversification may offer little protection from market declines, it is especially salient in cases of a worldwide recession – while the average individual country’s returns after such an event tend to stay depressed, global portfolios go on to eventually recover. In other words, while global diversification may not necessarily provide protection from the initial crash, it does create the potential for a significantly faster recovery. And this behavior tends to be more pronounced with longer time horizons – which are ultimately more relevant for investors with long-term wealth goals.

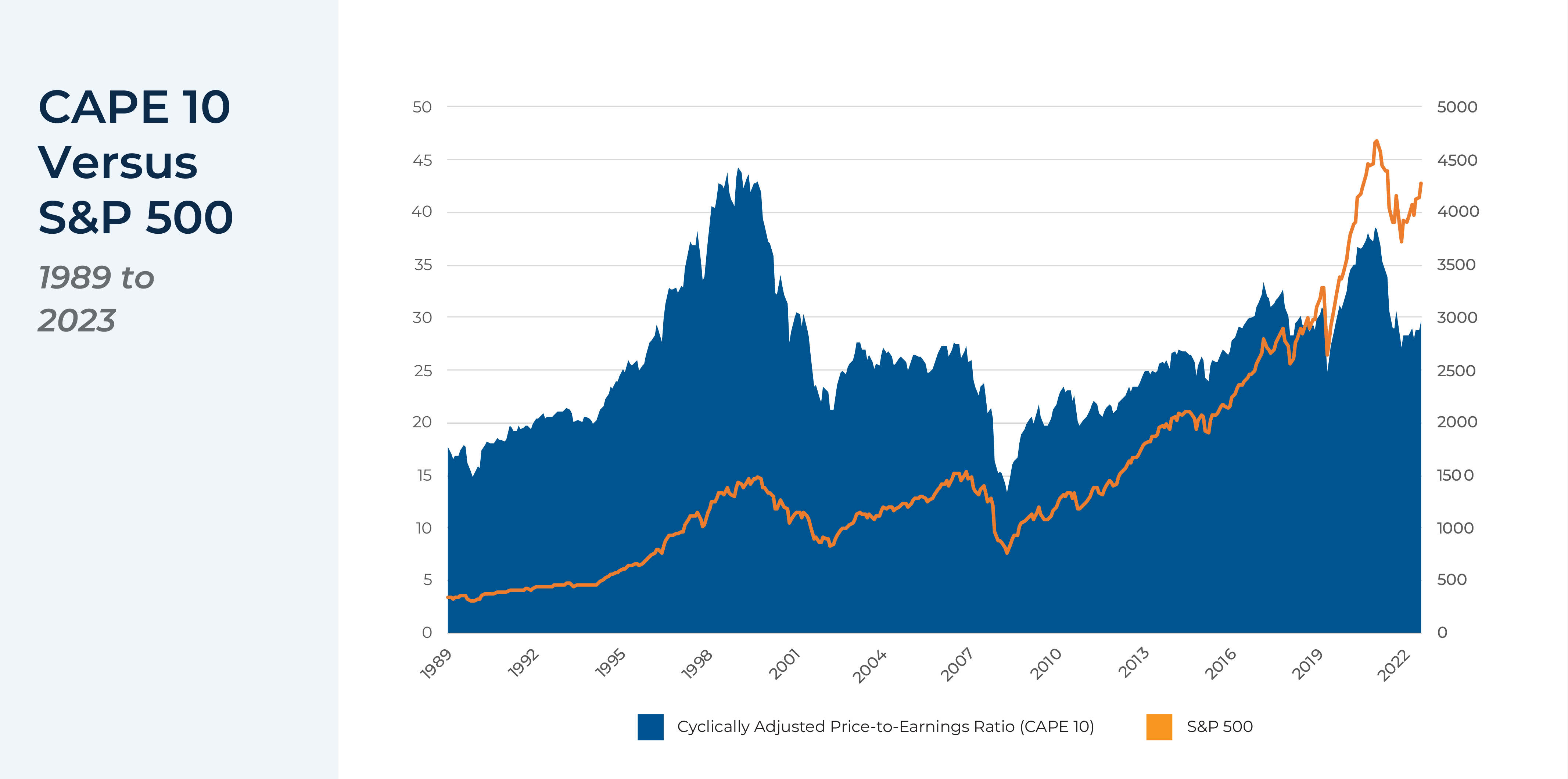

In addition to overlooking global long-term recovery patterns, investors often fail to consider the important role that valuation changes play in investment returns. Despite the caveat that “past performance is no guarantee of future results”, the patterns of historic past earnings data can offer insight into how a company is valued, which can influence the performance of its shareholders’ equity. For example, a strong case has been made for the predictive value of the CAPE 10, a price-to-earnings metric designed to assess relative market valuation, which is especially insightful when it comes to long-term returns. As while investment returns can be driven by underlying economic performance, such as through growth in earnings, they can also be driven by changes in valuations. And even though timing markets based on valuations in the short-term has not proven to be a successful strategy, the CAPE 10 has been positioned as a useful predictor of long-term future returns. Given the current (as of March 2023) economic positions for the U.S. CAPE (at 3.4%) and the EAFE CAPE 10 (5.6%), unless these values change, investors can reasonably estimate EAFE markets to outperform the S&P 500 by 2.2% annually.

Ultimately, the key point is that when evaluating for diversification, many investors can be prone to behavioral biases that preclude them from maintaining a well-diversified risk-appropriate portfolio that relies on a mix of U.S. and global investments. But by helping clients develop a clear understanding of the actual risks of diversification and a healthy perspective of historical market performance, advisors can prepare their clients to stay disciplined and focused on long-term results, ending out as both more informed and more insulated against inevitable market dips!

{kind=link}