Late last year, Zillow said home prices needed to come down about 25% to become affordable again.

Around that same time, mortgage rates hit their highest point in 20 years, with the 30-year fixed surging above 7%.

That led many to draw the conclusion that relief was in sight, at least if you were a prospective home buyer.

And indeed, home prices did fall shortly after, coming down 3.3% in March, per Redfin, the largest year-over-year decline since 2012.

But that was then, and this is now. In May, home prices hit a new all-time record high. What on Earth is going on?

After a Brief Pause, Home Prices Are Reaccelerating

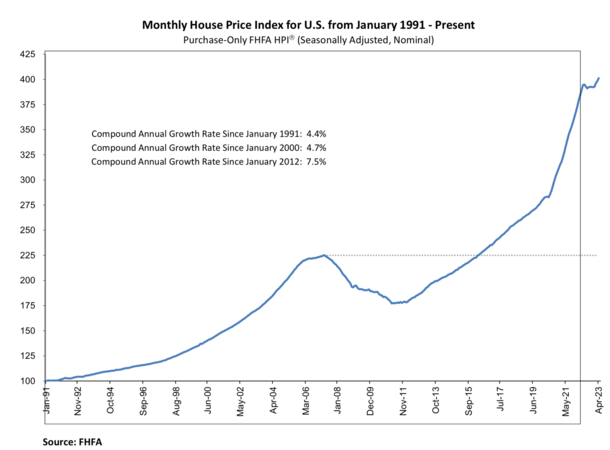

The pandemic-fueled housing market is the stuff of legends. Just look at this chart from the FHFA, which oversees Fannie Mae and Freddie Mac.

Home prices had already surpassed the prior housing bubble peak before COVID-19 reared its ugly head.

But just look how much higher they climbed from 2020 onward. This explosive growth worried the Fed, which was also dealing with out-of-control inflation.

And led to Federal Reserve Chairman Jerome Powell calling for a housing market “reset,” which he believed could be accomplished via countless interest rate increases.

As noted, it did indeed lead to a massive spike in mortgage rates, with the 30-year fixed more than doubling from the low-3% range to over 7% by late 2022.

Eventually, that did dampen home prices, with some reporting it as the second largest home price correction of the post-WWII era.

Problem is, it was short-lived, and if you consider how much home prices went up prior to the correction, it was a drop in the bucket.

Yes, some areas of the country have fared worse than others, but most markets nationwide have proven to be quite resilient.

This has a lot of housing bears, renters, prospective buyers, and economists in general scratching their heads, wondering why home prices aren’t dropping.

There’s Still No Housing Supply Out There

One of the major themes in the housing market since prices bottomed in 2012 has been a lack of supply.

And it really hasn’t changed much since then. In fact, by some measures housing inventory has worsened.

For example, Redfin reported last week that months of supply was a mere 2.6 months, close to its lowest level in a year.

Similarly, Black Knight noted that for-sale inventory has improved “modestly,” but remains 51% off pre-pandemic levels.

Generally, four to five months is considered a balanced market, with less supply tipped in favor of sellers as opposed to buyers.

As to why, there’s been a shortage of homes for sale since the 2010s, generally due to underbuilding. Further exacerbating that shortage has been the so-called mortgage rate lock-in effect.

Simply put, most homeowners have 30-year fixed-rate mortgages set at 2-3% (or even sub-2%), effectively locking them into their homes.

This is either because they can’t leave (due to a lack of affordability) or because they choose not to (they don’t want to buy a replacement home with a 7% mortgage).

Taken together, there are simply not enough homes on the market, despite decreased demand from buyers.

Yes, demand is also down, as the Fed expected it to be, due to much higher mortgage rates. And still-high home prices.

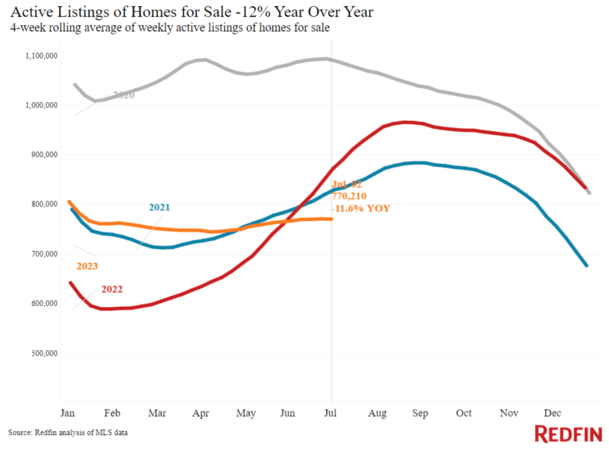

But because supply is also so low, with active listings down 12% year-over-year, low demand isn’t enough to push down home prices.

That’s an important thing to highlight because the housing market isn’t particularly hot. It’s just a lack of supply that’s keeping things together.

But Affordability Has Never Been Worse!

Those rightfully critical of sky-high home prices have pointed to historically bad affordability.

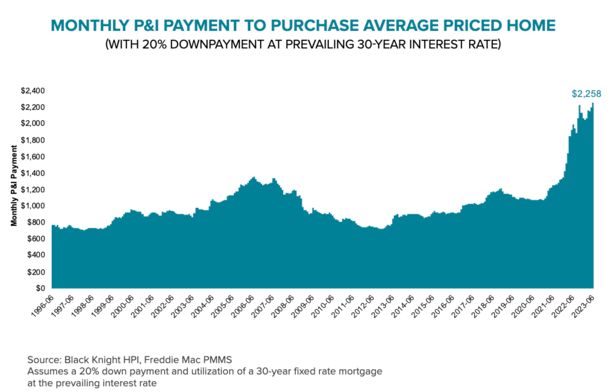

Lofty asking prices and much higher mortgage rates require a $2,258 monthly principal and interest payment on a median-priced home with 20% down and a 30-year mortgage set at 6.67%.

This is the highest payment on record, per Black Knight, and up markedly from levels seen just a few years prior.

In Los Angeles, 68% of median income is required to buy the average home, which is clearly too much.

Black Knight pointed out that we’d need a 30% drop in home prices to get back to “normal affordability.”

The alternative is 19% income growth if home prices remain flat and mortgage rates fall to 5%.

In the meantime, home prices are simply too high from an affordability standpoint, which explains weak demand.

But because supply remains constrained, home prices defied expectations and chalked an impressive 0.7% month-over-month gain in May.

That could put annual appreciation close to 9% again, which would be seemingly ridiculous given the high mortgage rates currently on offer.

However, we need to remember that home prices and mortgage rates aren’t negatively correlated. Both can rise or fall together.

For example, the economy could fall into a recession, pushing mortgage rates down while also driving property values lower.

Or the reverse could happen. A robust economy, similar to the one we’re in now, could push interest rates up and home prices along with it.

In other words, you need a catalyst to tank home prices, such as massive unemployment, which has yet to materialize.

Some Housing Markets Faring Worse Than Others

While national home prices appear to have resumed their upward trajectory, after a very brief pause, not all housing markets are performing the same.

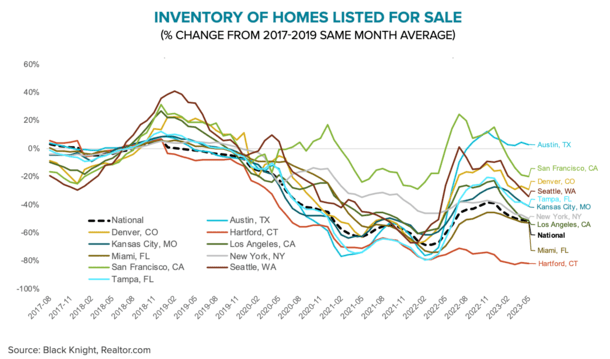

The worst at the moment is once-hot Austin, Texas, where prices are off a sizable 13.8% from their peak.

Interestingly, “inventory there continues to run above pre-pandemic levels,” which might kind of sum up the situation nationally.

In places where inventory hasn’t declined (or worse, risen), home prices are under pressure, which is logical given affordability issues.

But per Black Knight, so far this year active listings have fallen in 95% of major metros and remain 50% lower than pre-pandemic levels.

So other markets that were struggling, such as Seattle and San Francisco, have bounced back as their inventory has swung from oversupply back to undersupply.

This might explain why home prices aren’t dropping, even with 7% mortgage rates.

Keep an eye on inventory, and less on mortgage rates, to determine where home prices go next.

{kind=link}