Company Overview:

Utkarsh CoreInvest Limited, the bank’s promoter, started as a microfinance-focused non-banking financial company (NBFC) in 2010, catering to underserved areas in Uttar Pradesh and Bihar. The bank’s headquarters is in Varanasi, Uttar Pradesh, and it has strategically expanded its SFB (Small Finance Bank) operations in states where Utkarsh CoreInvest had prior microfinance experience. The bank received the RBI License in 2016, allowing it to establish and operate as an SFB. Their products encompass microbanking loans, including joint liability group loans and individual loans. They also provide retail loans, both unsecured (business loans and personal loans) and secured loans (loans against property). Additionally, they offer wholesale lending facilities to SMEs, mid to large corporates, and institutional clients, along with housing loans focused on affordable housing, commercial vehicle/construction equipment loans, and gold loans that were introduced in Fiscal 2022.

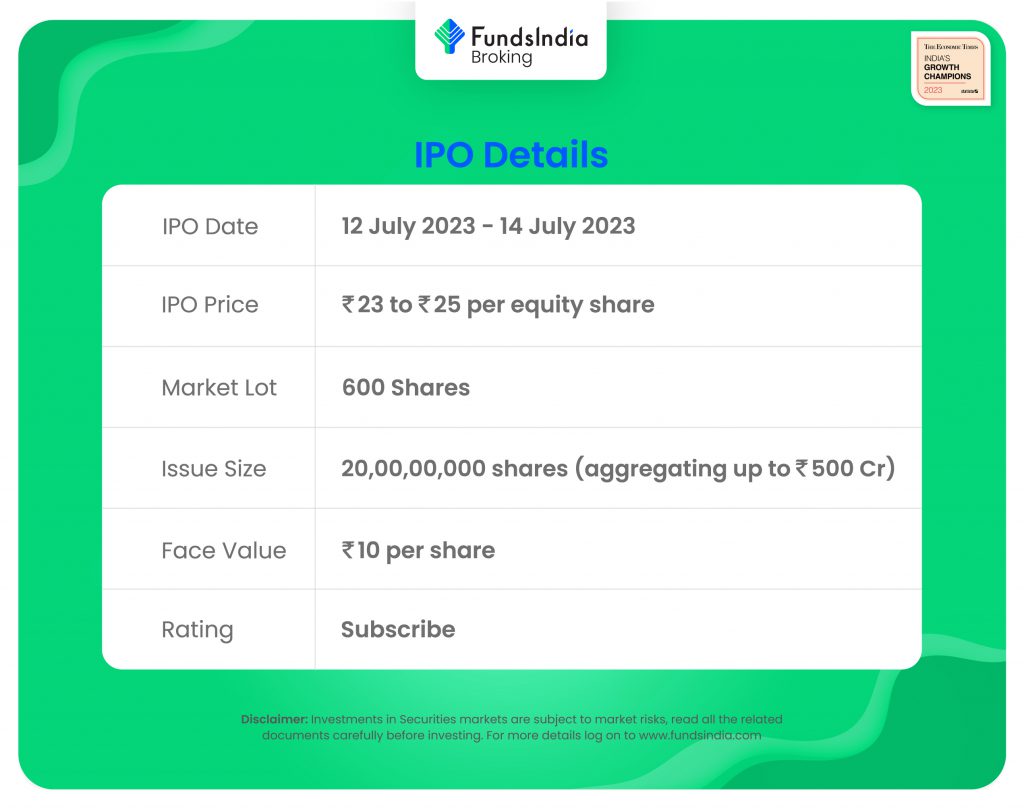

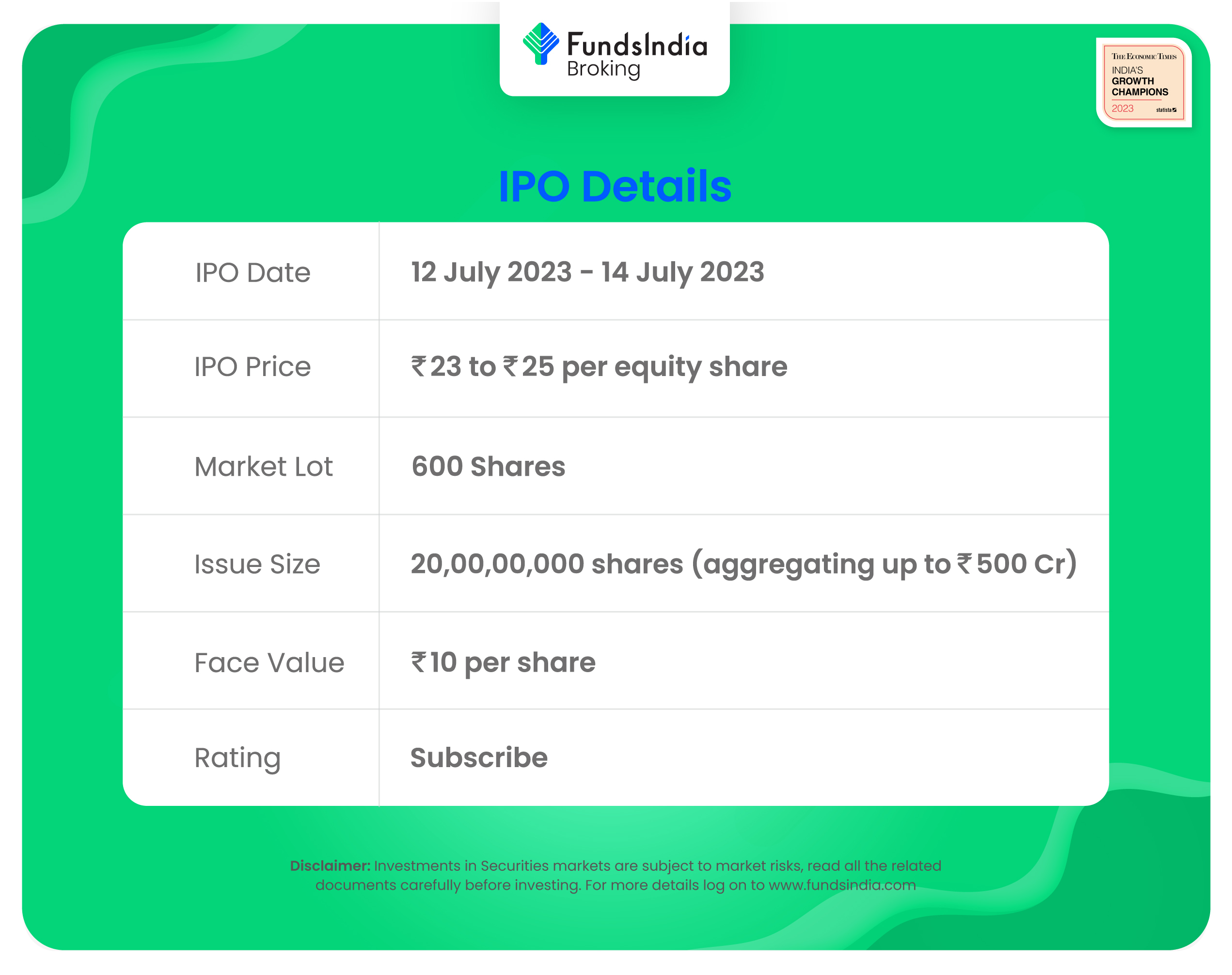

Objects of the Offer:

- Bank proposes to utilize the Net Proceeds from the Issue towards augmenting its Tier – 1 capital base to meet its future capital requirements.

- Achieve the benefits of listing the Equity Shares on the Stock Exchanges.

Investment Rationale:

- Robust Loan Growth: As of March 31, 2023, Utkarsh SFB operates across 26 states and union territories, with 830 banking outlets and 15,424 employees. The majority of its banking outlets are located in rural and semi-urban areas, surpassing the regulatory requirement of 25% for SFBs. With a customer base of 3.59 million, the bank focuses on rural and semi-urban regions, particularly in Bihar and Uttar Pradesh, where it has a strong asset quality and moderate credit penetration. TheGross Loan Portfolio has grown from Rs.8416 crs as of March 31, 2021 to Rs.10631 crs as of March 31, 2022 and further to Rs.13957 crs as of March 31, 2023. The bank recorded the third fastest Gross Loan Portfolio growth of 31% CAGR between FY 2019 and FY 2023 among SFBs with Gross Loan Portfolio of more than Rs.6000 crs (Source: CRISIL Report). The disbursements increased from Rs.5914 crs in FY 2021 to Rs.9046 crs in FY 2022, and was Rs.12443 crs in FY 2023. The deposits have also grown consistently and were Rs.7508 crs as of FY21, Rs.10074 crs as of FY22 and Rs.13710 crs as of FY23. CASA to total deposits ratio was 17.68% as of FY21, increased to 22.37% as of FY22, and further to 20.89% as of FY23.

- Prudent Risk Management: Risk management runs at the core of the bank’s operations and it has focused on robust and comprehensive credit assessment and risk management framework. The banks’ framework identifies, monitors and manages risks inherent to its operations and in particular manages credit, liquidity, market, IT and operational risks. have a comfortable liquidity profile that is backed by shorter tenure microbanking lending and sufficient liquidity buffer and as of March 31, 2023, the Liquidity Coverage Ratio (“LCR”) was 375.82% as against regulatory requirement of maintaining LCR of 90%.

- Financial Track Record: The Interest earned has been consistently growing and grew from Rs.1589 crs in FY21 to Rs.1849 crs in FY22 and further to Rs.2505 crs in FY23. The Net Interest Income (NII) in FY21, FY22 and FY23 was Rs.839 crs, Rs.1061 crs and Rs.1529 crs, respectively. The Net Interest Margin in FY21, FY22 and FY23 was 8.20%, 8.75% and 9.57%, respectively. The net profit for the year, as restated, for FY21, FY22 and FY23 was Rs.112 crs, Rs.61 crs and Rs.404 crs, respectively. As a result of strong performance, the return on total average assets was 1.05%, 0.48% and 2.42%, as of March 31, 2021, 2022 and 2023, respectively, while the return on average equity was 9.99%, 4.14% and 22.84%, respectively. The Net NPA (NNPA) of the bank has improved from 1.33% in FY21 to 0.39% in FY23.

Key Risks:

- Regulatory Risk – The bank is subject to inspections by regulatory authorities like RBI.Noncompliance with RBI inspections/observations or other regulatory requirements, as well as any negative observations from such regulators, may have a material adverse effect on the business, financial condition, operating performance, or cash flows.

- Client Concentration Risk – A significant portion of the advances in the micro banking segment are towards customers located in the states of Bihar and Uttar Pradesh, and any adverse changes in the conditions affecting the region can adversely impact the company’s business, financial condition, results of operations and cash flows.

Outlook:

The IPO is a complete fresh issue (100%) which is key positive for the company. The adjusted EPS (including the fresh issue) is Rs.3.69 for FY23 and the adjusted book value for FY23 stands at Rs.22.8. According to RHP, the listed peer group of the bank are Equitas Small Finance Bank Limited, Ujjivan Small Finance Bank Limited, AU Small Finance Bank Limited, Suryoday Small Finance Bank Limited, etc. At the higher price band, the listing market cap will be around ~Rs.2740 crs and the bank is demanding a P/E multiple of 6.7x based on FY23 EPS and a P/B multiple of 1.1x. The peers are trading at an average P/B of 2.4x with 4.7x as the highest number. When compared to its peers, Utkarsh Small finance bank looks undervalued. Based on the above views, we provide a ‘Subscribe’ rating for this IPO.

If you are new to FundsIndia, open your FREE investment account with us and enjoy lifelong research-backed investment guidance.

Other articles you may like

{kind=link}

{kind=link}