In late 2019, Congress passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act, introducing several significant changes to retirement planning. Of the many provisions in the bill, the so-called “Death of the Stretch” arguably received the lion’s share of consternation from the financial advisor community. Under the new law, non-spouse beneficiaries (with few exceptions) must now withdraw the entirety of an inherited IRA within 10 years of the account owner’s passing rather than over their own lifetimes. This shift has led financial advisors to explore new strategies for mitigating the resulting tax-planning challenges. One effective approach is the use of a Testamentary Charitable Remainder UniTrust (T-CRUT). As a non-person entity, the T-CRUT is not subject to the 10-Year Rule and can be designated as the IRA beneficiary while naming the original non-spouse beneficiary as an income recipient of the trust and a charitable organization as the remainder beneficiary. This allows the account to grow on a tax-deferred basis, with income to beneficiaries being taxed when distributions are made.

In this guest post, Kathleen Rehl, a “reFired” financial planner and author of “Moving Forward on Your Own: A Financial Guidebook for Widows”, shares her story of how (and why) she used a T-CRUT to create, upon her passing, a steady stream of income for her son, thus preserving the wealth of his legacy over time, avoiding the income tax burden that he would potentially encounter as the sole beneficiary of her IRA, and leaving a portion of that account to various nonprofits she supports.

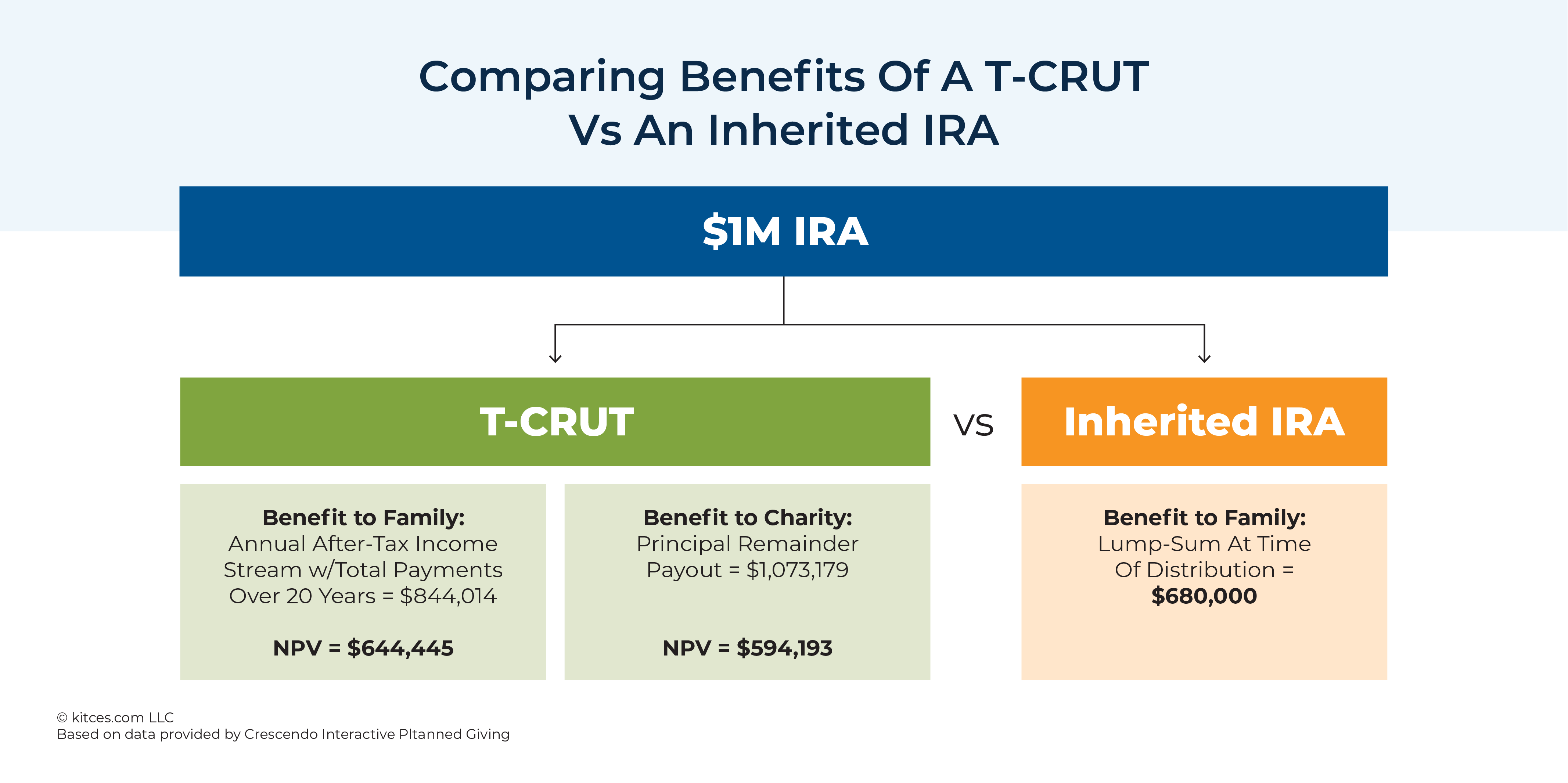

Notably, her strategy to preserve her son’s wealth while meeting her own charitable goals relies on 4 key principles. First is that the underlying vehicle is a Charitable Remainder UniTrust (CRUT), which pays a fixed percentage of the trust’s value for either a specified number of years (not to exceed 20) or through the lifetime of the beneficiary. Second is that the CRUT is testamentary (i.e., it is an ’empty basket’ that doesn’t receive funds until the owner’s passing). Third, the IRA assets are directed to the T-CRUT as its funding source upon her passing, and fourth, that, at the end of the specified period, a minimum of 10% of the initial fair market value of the assets placed within the trust is transferred to a qualified charity (or charities) as the final remainder beneficiary.

While such a strategy may not provide the same level of after-tax benefit to her son if he were to inherit her IRA outright (where he would be faced with the temptation to empty the account and spend the proceeds immediately), the T-CRUT strategy ensures her son’s financial security through an annual income stream lasting into his retirement as well as leaving a charitable legacy that matches her values. As such, while leaving funds in an IRA may be the better option for those seeking to maximize wealth, using a T-CRUT to preserve wealth for a beneficiary while meeting philanthropic goals can be a very appealing solution.

Ultimately, the key point is that there are a number of tools that financial advisors can use to help their clients’ beneficiaries circumvent the tax burden (as well as other potential challenges) associated with inheriting retirement accounts. More importantly, using various tax-efficient “Give It Twice” charitable tools allows financial advisors to help their clients create comprehensive estate plans that can benefit both their loved ones and the causes that are most meaningful to them!

{kind=link}