Larsen & Toubro Ltd – Building a Better World

Headquartered in Mumbai, Larsen & Toubro Ltd. (L&T) provides capabilities across Technology, Engineering and Manufacturing. A strong, customer-focused approach and the constant quest for top-class quality have enabled L&T to attain and sustain leadership in its major lines of business for over eight decades. It has been a part of many strategically important projects such as construction of India’s longest sea bridge Shri Atal Bihari Vajpayee Trans Harbour Link, Shri Ram Janmabhoomi Mandir in Ayodhya, ongoing Hyderabad Metro construction and so on. It operates in over 50 countries worldwide. The company’s manufacturing footprint extends across eight countries in addition to India.

Products and Services

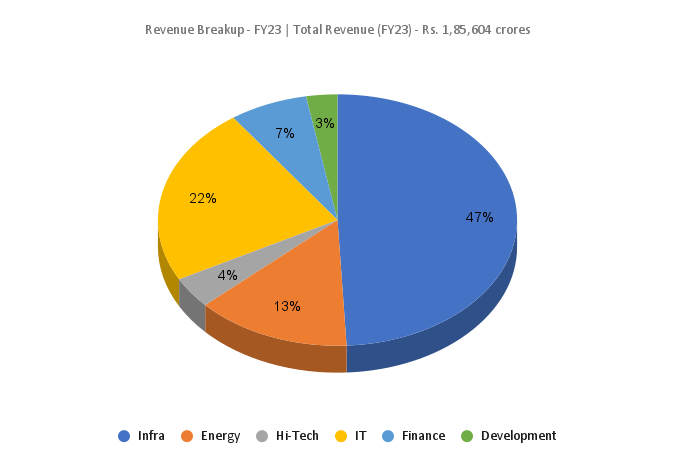

L&T operates across the following business segments: Infrastructure projects (Buildings & factories, heavy civil, water, power T&D, transport, metals & minerals), Energy projects (Hydrocarbon, power, green energy EPC), IT & TS (LTIMindtree, LTTS, Digital Platforms, Data Centres, Semiconductor Design), Hi-Tech Manufacturing, Financial Services, Development projects and other services.

Subsidiaries: As of March 31, 2023, the L&T Group comprised 92 subsidiaries, 5 associate companies, 27 joint ventures and 35 jointly held operations.

Key Rationale

- Performance of Infra segment – L&T was the major EPC contractors behind the construction of the prestigious Atal Setu, which is India’s longest sea bridge. The company also constructed the Ram Mandhir in Ayodhya. As of 31 December 2023, infrastructure segment has a prospect pipeline of Rs.4.10 trillion. Order inflows of the infra segment secured orders of Rs.432 billion for Q3FY24 vis-a-vis Rs.325 billion in Q3FY23 representing a growth of 33% over the corresponding quarter of the previous year.

- Performance of energy segment – On the Green Energy side, L&T Electrolysers Limited has emerged as a successful bidder with an allotted capacity of 63 MW under the tranche-I of the PLI scheme for electrolyser manufacturing, launched by the Ministry of New and Renewable Energy. For the energy segment there is a strong order prospects pipeline of Rs.2.01 trillion, comprising Hydrocarbon prospects of Rs.1.7 trillion and Power prospects of Rs.0.3 trillion. In the UAE, the business has received an order for engineering, supply, construction, installation, testing and commissioning a 400/132kV substation. In Kuwait, the business won an order to establish 400kV overhead transmission lines and the associated 400kV underground cable interconnections. L&T has also bagged an order to set up a 75 MW floating solar photovoltaic plant on a dam which is a part of the ultra-mega renewable energy power park, being developed on Damodar Valley corporation reservoirs in Jharkhand and West Bengal.

- Performance of IT segment – The company has two listed entities in the IT segment – LTIMindtree and LTTS. The revenues for this segment at Rs.112 billion in Q3FY24 registered a modest growth of 5% largely in line with the subdued global macro conditions impacting IT spends. The voluntary attrition in both listed entities, LTIMindtree and LTTS has reduced both on a sequential and YoY basis.

- Q3FY24 – During the quarter, the company reported revenue of Rs.55,128 crores, an increase of 19% YoY compared to the Rs.46,390 crores of Q3FY23. EBITDA increased by 14% YoY to Rs.5,760 crores. Net profit improved by 19% from Rs.3,058 crores in Q3FY23 to Rs.3,593 crores in Q3FY24. Order inflow increased by 25% during the quarter, aided by strong capex momentum in the Middle East. International orders constituted 39% of the December 2023 order book.

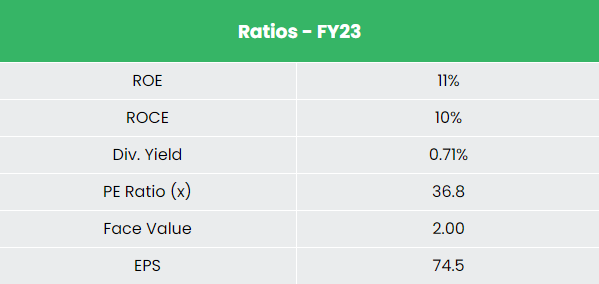

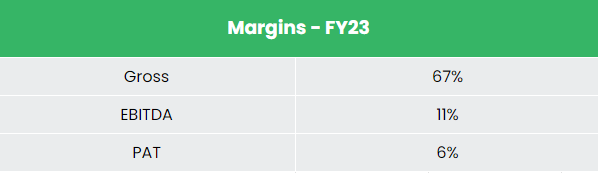

- Financial performance – The company has generated revenue and PAT CAGR of 9% and 3% over the period of 5 years (FY18-23). In the trailing twelve months (TTM) revenue and PAT growth stood at 19% and 26%. Average 5-year ROE & ROCE is around 14% and 11% for FY18-23 period.

Industry

India’s high growth imperative in 2024 and beyond will significantly be driven by major strides in key sectors with infrastructure development being a critical force aiding the progress. The country has to enhance its infrastructure to reach its 2025 economic growth target of US$ 5 trillion. India’s population growth and economic development require improved transport infrastructure, including investments in roads, railways, and aviation, shipping and inland waterways. The US$ 1.3 trillion national master plan for infrastructure, Gati Shakti, has been a forerunner to bring about systemic and effective reforms in the sector, and has already shown a significant headway.

Growth Drivers

In Budget 2023-24, capital investment outlay for infrastructure is being increased by 33% to Rs.10 lakh crore (US$ 122 billion), which would be 3.3 per cent of GDP. As per the Union Budget 2023-24, a capital outlay of Rs. 2.40 lakh crore (US$ 29 billion) has been provided for the Railways, which is the highest ever outlay and about 9 times the outlay made in 2013-14. Infrastructure Finance Secretariat is being established to enhance opportunities for private investment in infrastructure that will assist all stakeholders for more private investment in infrastructure, including railways, roads, urban infrastructure, and power.

Competitors: Rites Ltd, IRB Infrastructure Developers Ltd etc.

Peer Analysis

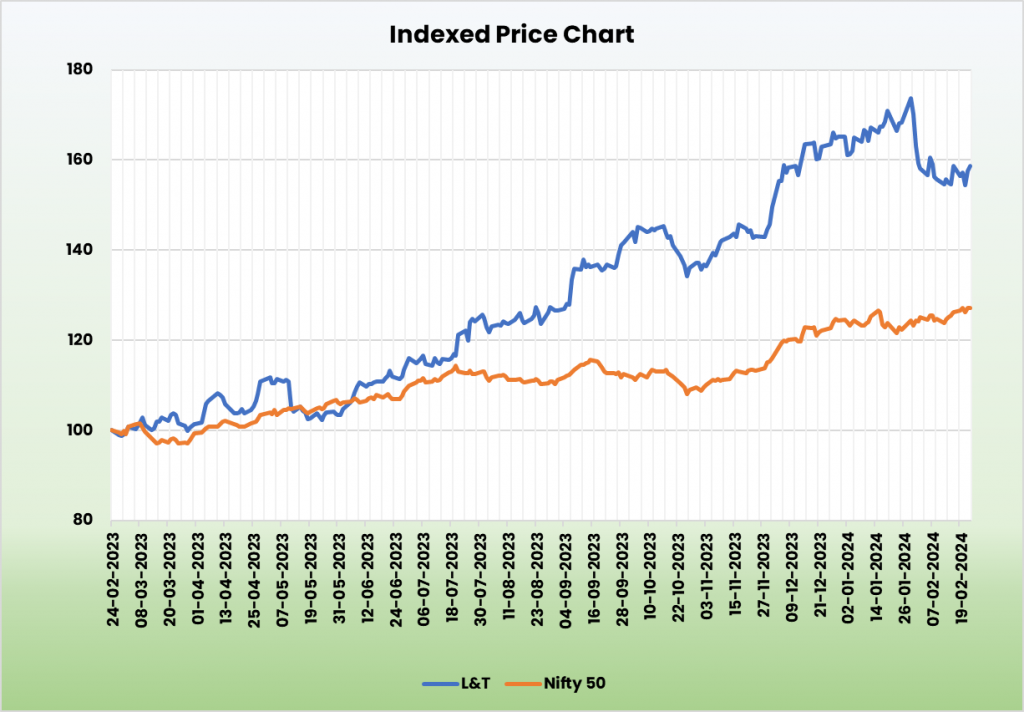

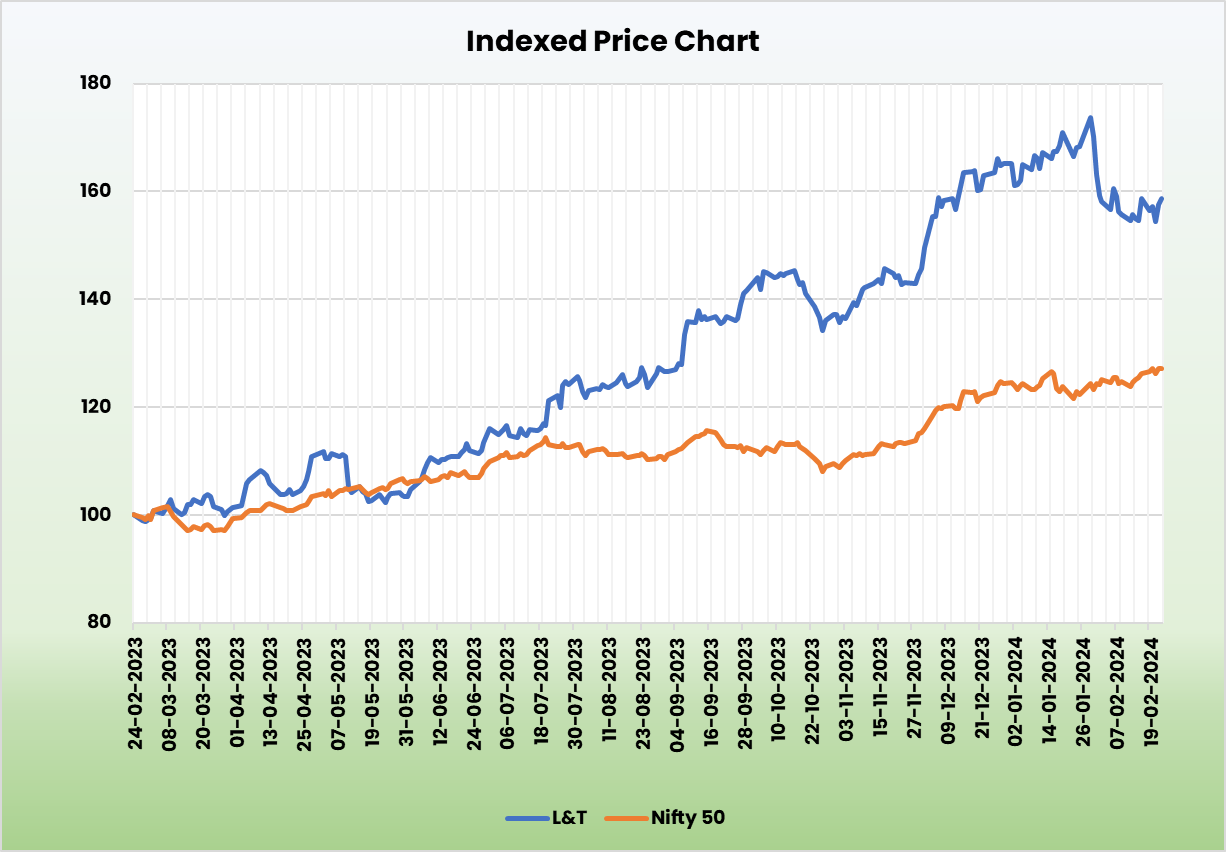

Compared to the above competitors, L&T has generated higher return ratios in line with the growth in the sales. This indicates the company’s ability to generate better profits for the capital invested.

Outlook

The company has robust order pipeline of Rs.6.3 trillion in the near term. The group is stepping into two new business – Green Hydrogen and Data Centre. The company is looking forward to having an aggregate capacity of around 60 MW in the Data Centre domain over the next couple of years. It manufactured its first electrolyser of 1 MW in the Hazira factory during the quarter. Also, during, L&T converted related party debt to equity in Hyderabad Metro leading to a savings of Rs.240 crores in interest costs. It also incorporated an additional wholly owned subsidiary with an aim to engage in the business of fabless semiconductor chip design and product ownership.

Valuation

L&T is a strong player in India’s capex spend for infrastructure development and execution of the nation’s strategic projects. We expect the company to retain its leadership position in the mid to long term as well. We recommend a BUY rating in the stock with the target price (TP) of Rs. 3,997, 30x FY25E EPS.

Risks

- Forex Risk – The company has significant operations in foreign markets and hence is exposed to forex risk. Any unforeseen movement in the forex market can adversely affect the company.

- Project execution delay – Any delay in timely execution of orders might impact the revenue and profit estimates.

Other articles you may like

{kind=link}

{kind=link}

{kind=link}