According to the Federal Reserve Board’s July 2024 Senior Loan Officer Opinion Survey (SLOOS), lending standards were essentially unchanged for all residential real estate (RRE) categories in the second quarter of 2024. However, demand for RRE loans remained modestly weaker across all categories in the quarter. Lending conditions were significantly tighter, and loan demand modestly was weaker across all commercial real estate (CRE) loan categories. Nevertheless, language from the most recent Federal Open Market Committee (FOMC) suggest that cuts to the federal funds rate are imminent which will be welcomed relief for the real estate market and will help stimulate future loan activity.

Residential Real Estate (RRE)

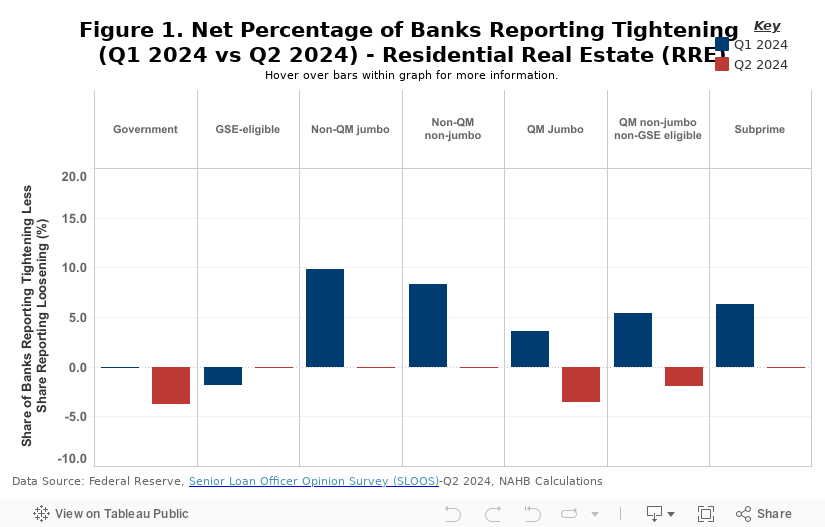

Four of the seven RRE categories (GSE-eligible, non-Qualified Mortgage or QM jumbo, Non-QM non-jumbo, and Subprime)recorded a net share of banks reported tighter lending standards in Q2 2024 as neutral (i.e., 0%) . The other three categories, which included government (i.e., issued by FHFA, Department of Veteran Affairs, USDA, etc.), QM jumbo, and QM non-jumbo non-GSE eligible recorded a negative reading which means that more banks reported looser rather than tighter conditions.

Six of the seven categories of RRE loans showed a decrease in net tightening from Q1 2024 to Q2 2024, with the only exception being GSE-eligible which increased 1.8 percentage points. The largest drop in the net tightening percentage occurred for Non-QM jumbo which fell 9.8 percentage points (pp) from 9.8% in Q1 2024 to 0% in Q2 2024.

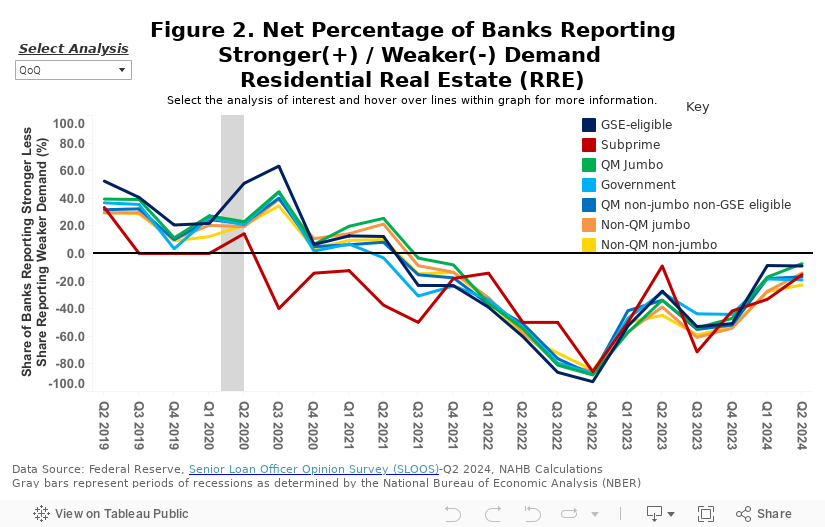

All RRE categories reported net weaker demand in Q2 2024. The survey has shown that banks have indicated weaker demand for at least 12 consecutive quarters for all RRE categories going back to Q2 2021 (Subprime leads all RRE categories at 16 consecutive quarters).

Commercial Real Estate (CRE)

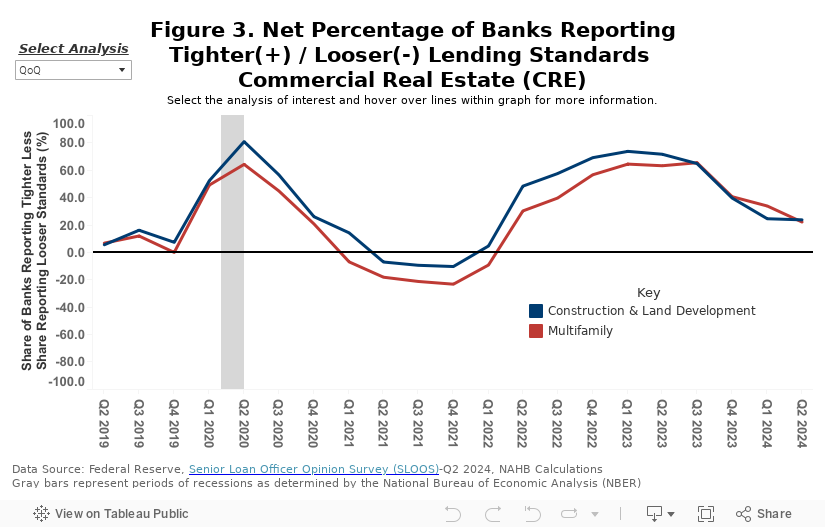

Banks reported significantly tighter lending conditions for both multifamily as well as all CRE construction & development loans in Q2 2024. However, both categories showed less net tightening than they did a quarter before, most noticeably multifamily falling 11.7 percentage points. Nevertheless, it has been 10 consecutive quarters of tighter lending conditions for construction & development and 9 consecutive quarters for multifamily.

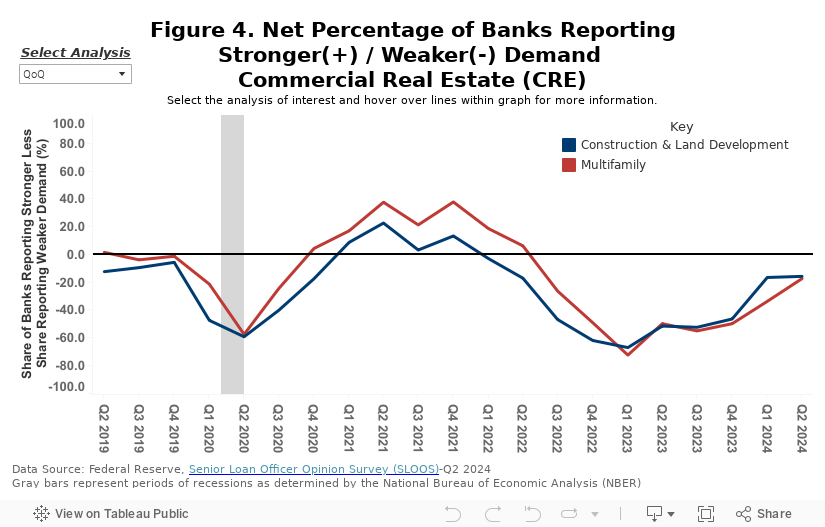

For multifamily, 17.5% of banks reported net weakening of demand for loans which is 16.4 percentage points lower compared to Q1 2024. As for construction & development loans, 15.9% of banks reported net weakening of demand for loans which was little changed from the previous quarter. Weaker demand has persisted for roughly the last two years for construction & development (10 consecutive quarters) and multifamily (8 consecutive quarters).

Special Questions

The Federal Reserve included a set of special questions this quarter which asked banks “to describe the current level of lending standards at your bank relative to the range of standards that has prevailed between 2005 and the present.” Effectively, they are asking banks to think about the median lending standards over the last two decades and determine where do conditions today rank on this continuum. On balance, banks indicated that the current level of lending standards is located at the tighter end of this range for all loan categories, including CRE and RRE loans.

Discover more from Eye On Housing

Subscribe to get the latest posts sent to your email.

{kind=link}