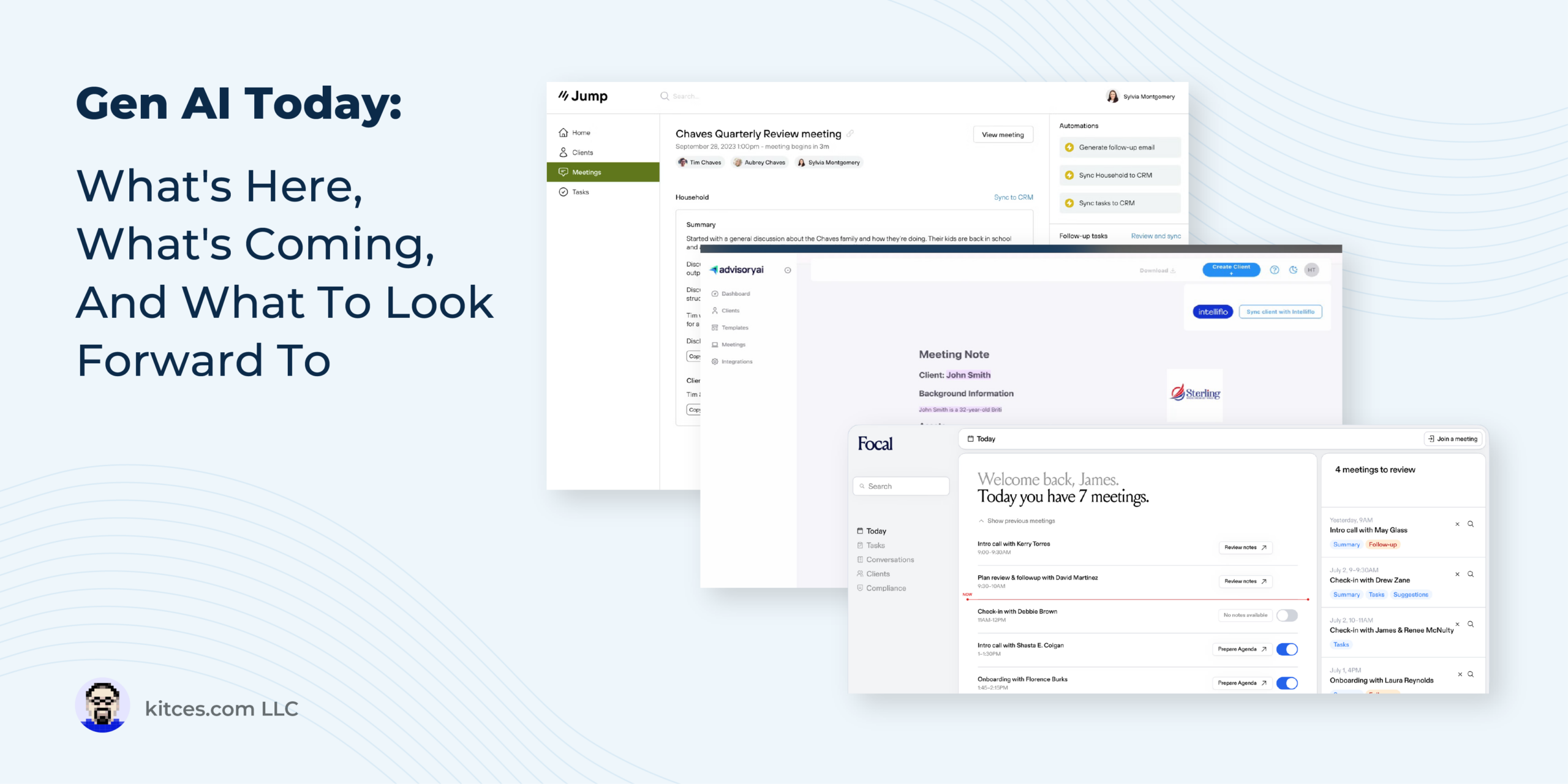

In the nearly 2 years since the launch of ChatGPT, there has been an explosion of new technology solutions incorporating Artificial Intelligence (AI). Today, AI is now almost ubiquitous across many of the tools that we use, from smartphone cameras to search engines to office productivity software. For financial advisors, too, a ballooning number of new advisor-focused AI tools has appeared over the last 24 months, purporting to save advisors’ time and staffing needs by automatically performing previously manual tasks like creating meeting agendas, generating marketing materials, and even analyzing and recommending financial planning strategies.

And yet, despite the flood of new AI tools and the assurances that advisors hear from software providers and AI proponents that AI will soon prove to be life-changing in its ability to ‘intelligently’ perform any task that the user asks of it, the impact that AI will have in the long term is still unclear. Much like how other forms of technology in the past 30 years (such as online shopping in the early internet era and blockchain solutions in the late 2020s) went through early hype phases only to have the bubble burst when many of the business models based on the new technology proved to be unsustainable, AI is going through its own speculative phase where new AI solutions are popping up for nearly every use case imaginable – except, as the lessons from previous technology bubbles have shown, many of the use cases currently being offered for AI won’t actually prove valuable enough to build successful solutions.

But the likelihood that many of today’s AI solutions may fall flat in the short term doesn’t necessarily mean that AI won’t ultimately bring significant benefits for advisors; it just means those benefits may take a long time –possibly a decade or more – to become evident. At least to some extent, this will be the result of generative AI’s ability to grow over time, as AI technology itself becomes more reliable and capable of a broader range of functions. Additionally, as it becomes clearer which AI use cases provide real value, those applications will gradually gain traction among advisors and may even become integral to how they serve clients and manage their businesses.

For the time being, however, it may be helpful for advisors to take a realistic approach to the value that AI tools will provide, especially in an environment where technology providers often make bold claims about their solutions’ ability to save time and reduce costs. Some of the capabilities of today’s AI tools (e.g., automating workflows or retrieving client information using a chatbot) may be useful to some extent, but if the processes that they replace don’t take that much time to begin with, then the tools’ benefits may not justify the additional cost to implement them. On the other hand, if the tool really does help advisors meaningfully cut the time they spend on inefficient tasks – such as client meeting preparation and follow-up – then they’re more likely to be worth the cost outlay.

The key point is that, like any technology, AI itself isn’t the solution to making advisors better and more successful; rather, it’s a foundation on which solutions can be built to help advisors address specific challenges while maximizing the technology’s current capabilities. For now, getting the most out of AI may mean focusing on more narrowly targeted AI solutions (rather than those offering a mosaic of tools, only some of which may hold real value) – as these are more likely to address the advisor’s actual needs, instead of trying to be the “One Solution” for everything, regardless of whether the problem truly needs solving!

{kind=link}