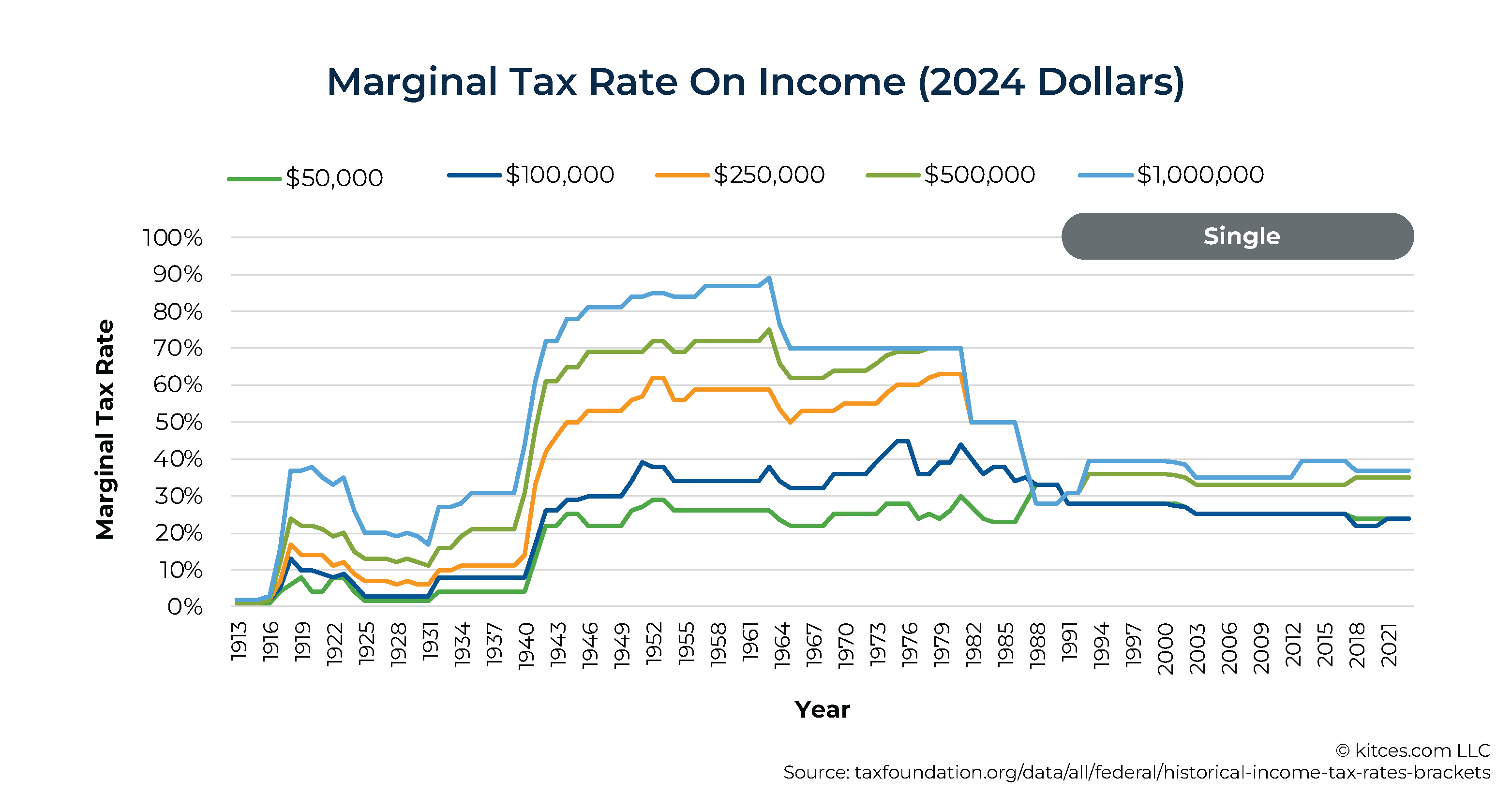

Over the last 60 years, the top Federal marginal tax bracket has steadily decreased from over 90% in the 1950s and 60s to ‘just’ 37% today. However, with the national debt expanding rapidly, observers of U.S. tax policy are predicting that Congress will inevitably be forced to again increase tax rates in order to raise revenue and balance the national budget – and that the current regime of relatively low tax rates will prove to be a temporary phenomenon.

From a financial planning perspective, the seeming implication of a likely rise in future tax rates would be that, given a choice between being taxed on income today or deferring that tax to the future, it makes more sense to be taxed today when taxes are lower than they’ll be in the future. For example, if taxes were expected to rise in the future, it would be better to contribute to a Roth retirement account (which is taxed on the contribution, but not upon withdrawal) than to a traditional pre-tax account (which is tax-deductible today but is taxable on withdrawal). As a result, there’s a common line of thinking that people saving for retirement should avoid pre-tax retirement accounts entirely and contribute (or convert existing pre-tax assets) to Roth instead – regardless of which tax bracket they’re in today.

While it’s true that the top marginal tax rate has decreased dramatically since the mid-20th century, the difference in the actual tax paid by most Americans has been far more modest. Because not only were very few households actually subject to the 1950s-era top tax rates (which were triggered at the equivalent of over $2 million of income in today’s dollars), but the long decline in nominal tax rates has also come with the elimination of many loopholes and deductions that have resulted in more income being subject to tax. Which means that it seems less likely that Congress will simply raise the marginal tax brackets in the future than that they will further reduce the benefits of current tax planning strategies – possibly including those of Roth accounts themselves!

Furthermore, focusing only on tax rates at a national level ignores the fact that an individual’s own tax rate is likely to change much more during their lifetime based on their own income and life circumstances. In particular, those nearing retirement may see a large swing from the upper tax brackets as they reach their peak earning years, to the lowest brackets upon retirement, and eventually stabilizing somewhere in the middle once they start receiving income from Social Security and Required Minimum Distributions (RMDs). Which creates a tax planning opportunity to make pre-tax contributions while in the peak earning years, and then to convert funds to Roth after retirement – and as long as those funds can be converted at a lower tax rate than they were contributed, it still makes sense to contribute them to a pre-tax account.

Ultimately, while the idea that we currently live in an anomalously low-tax environment that will inevitably reverse course has its appeal, basing one’s tax planning decisions around that assumption is still risky. Because even if taxes do creep up nationally, individuals who are already in the highest tax brackets today are still likely to be in a lower bracket upon retirement – which makes it better to contribute to a pre-tax account today and then withdraw (or convert) the funds at a lower rate later on!

{kind=link}