Company overview

Hyundai Motor India Ltd. (HMIL) is a part of the Hyundai Motor Group, the third largest auto original equipment manufacturer (OEM) in the world based on passenger vehicles sales in CY23. HMIL is the second largest auto OEM in the Indian passenger vehicles market since FY09 (in terms of domestic sales volume). The company has a portfolio of 13 models of passenger vehicle segments by body types such as sedans, hatchbacks, sports-utility vehicles (SUVs) and battery electric vehicles (EV). The company also manufactures parts, such as transmissions and engines that are used for its own manufacturing or sales. It is also the country’s second largest exporter of passenger vehicles. From 1998 to 30 June 2024, the company has cumulatively sold more than 12 million units of passenger vehicles in India and through exports. The company’s manufacturing facilities are located in Tamil Nadu, with a current production capacity of 824,000 (as of 30 June 2024).

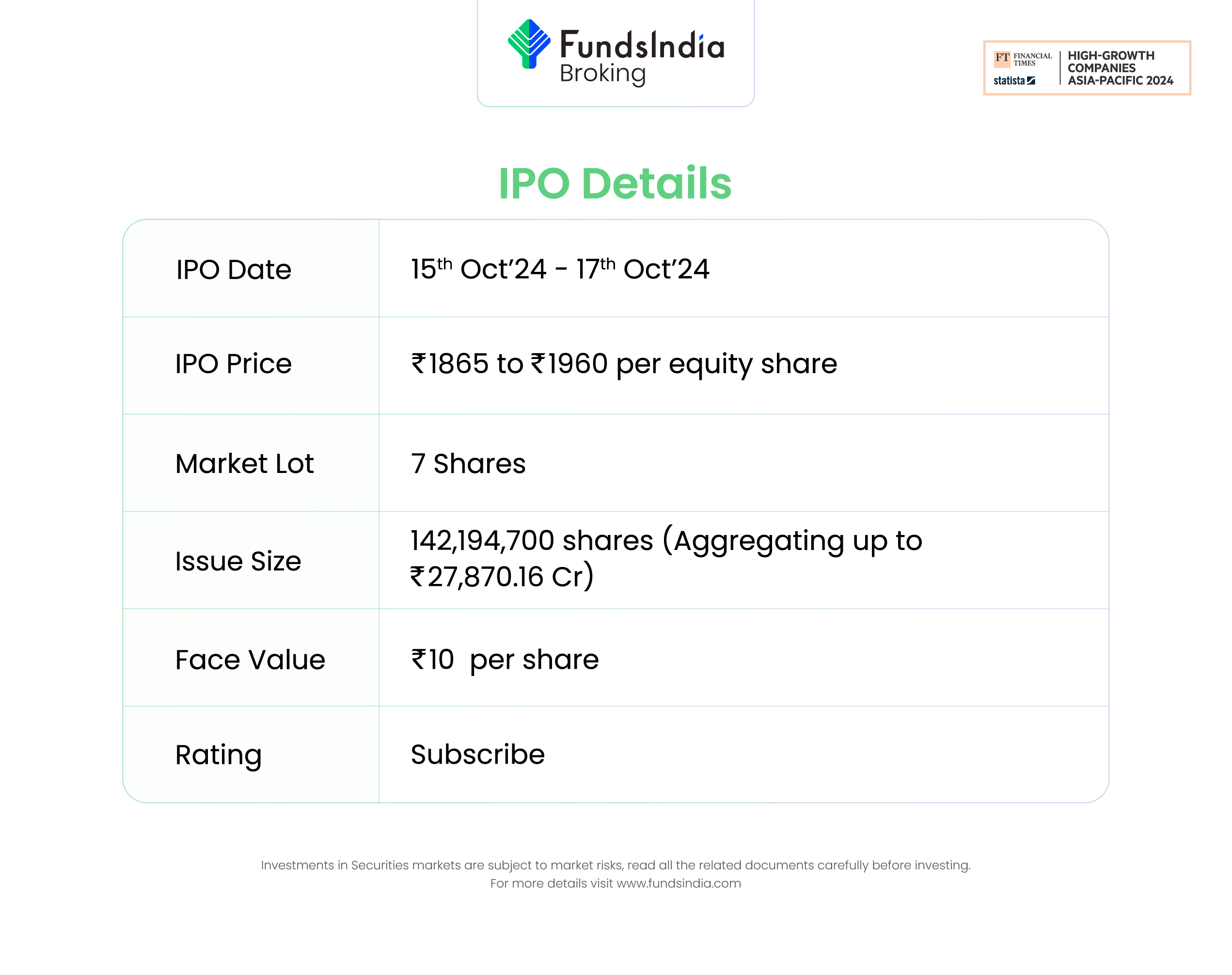

Objects of the offer

- Achieve the benefits of listing the Equity Shares on the Stock Exchanges.

- Carry out offer for sale of up to 142,194,700 Equity Shares by the Selling Shareholders.

Investment Rationale

- Strong parentage of Hyundai – The company gains significant advantages from its strong affiliation with Hyundai Motor Company (HMC). It benefits from various operational aspects, including management, research and development, design, product planning, manufacturing, supply chain development, quality control, marketing and distribution, brand value, and financing. Additionally, HMC’s extensive sales network, covering 190 countries, enhances the company’s export opportunities, which are vital for revenue. The company harness global insights and R&D capabilities to integrate technology, design, and aesthetics into passenger vehicles specifically tailored for the Indian market.

- Growth strategies – To address the increasing demand, the company is scaling its manufacturing capacity. As of June 30, 2024, it operates two manufacturing facilities in Tamil Nadu, with an annual production capacity of 824,000 units, running at nearly full capacity. During FY24, the company acquired the Talegaon Manufacturing Plant from General Motors India, to be operational in phases, with the first phase expected to be operational in H2FY26. The Talegaon Manufacturing Plant is an integrated passenger vehicle and engine manufacturing facility across approximately 300 acres of leased land allotted by the industrial development corporation premises. The company expects the annual production capacity across all the manufacturing plants in aggregate to increase to 994,000 units when the Talegaon Manufacturing Plant is partly operational and to 1,074,000 units once the Talegaon Manufacturing Plant is fully operational. With the addition of Talegaon plant, the company is aiming to boost production volume and accelerate economies of scale to match its supply chain capabilities in line with the growing demand in domestic as well as international markets.

- Financial Track Record – The company reported a revenue of Rs.69,820 crore in FY24 as against Rs.60,308 crore in FY23, an increase of 16% YoY. The revenue has grown at a CAGR of 21% between FY22-24. The EBITDA of the company in FY24 is at Rs.9,133 crore and EBITDA margin is at 13%. The PAT of the company in FY24 is at Rs.6,060 crore and PAT margin is at 9%. The CAGR between FY22-24 of EBITDA is 29% and PAT is 45%. The Return on Net Worth and Return on Capital Employed of the company stands at 12.26% and 13.69% as of 30 June 2024, respectively.

Key risks

- OFS risk – The IPO consists of only an Offer for Sale of up to 142,194,700 Equity Shares by the Selling Shareholders, Hyundai Motor Company. The entire proceeds from the Offer for Sale will be paid to the Selling Shareholders and the Company will not receive any such proceeds.

- Macroeconomic factors – Any slowdown in the household income due to macroeconomic factors might impact the demand and thereby the company turnover.

- Tech changes – The inability of the company to adapt to the rapidly evolving global automotive industry, leading to changes in technology utilization, might adversely affect the market share the company currently holds.

Outlook

The company benefits from the strong parentage of Hyundai Motors. The company has gained market position from (i) wide product offerings, (ii) stakeholder relationships and operations; (iii) the strong Hyundai brand in India; (iv) ability to leverage new technologies to enhance operational and manufacturing efficiency; and (v) ability to expand into new businesses such as EVs through innovation. According to RHP, Maruti Suzuki India Ltd, Tata Motors Ltd and Mahindra & Mahindra Ltd are the only listed competitor for Hyundai Motor India. The peers are trading at an average P/E of 23.57x with the highest P/E of 29.96x and the lowest being 11.36x. At the higher price band, the listing market cap of Hyundai Motor India will be around ~Rs.1,59,258 crore and the company is demanding a P/E multiple of 26.28x based on post issue diluted FY24 EPS of Rs.74.58. When compared with its peers, the issue seems to be fully priced in (fairly valued). Based on the above views, we provide a ‘Subscribe’ rating for this IPO for a medium to long-term Holding.

Other articles you may like

Post Views:

101

{kind=link}