Max Healthcare Institute Ltd – To excel, To serve

Incorporated in 2001, Max Healthcare is among India’s largest healthcare providers. With 22 facilities, 5,000+ beds, and 35,000+ employees, it operates across NCR Delhi, Haryana, Punjab, Uttarakhand, Maharashtra, and Uttar Pradesh. Its metro presence accounts for 81% of its bed capacity. The company also offers homecare (Max@Home) and diagnostics (Max Labs) services.

Products and Services

- Comprehensive healthcare services, including diagnostics, surgeries, critical care, and emergency services, with expertise in oncology, cardiology, orthopaedics, neurosciences, and more.

- Additional offerings include homecare, pathology, and preventive care services.

Subsidiaries: As of FY24, Max Healthcare operates 11 subsidiaries, including 2 step-down subsidiaries.

Growth Strategies

- Jaypee Healthcare Acquisition: Acquired a controlling stake in Jaypee Healthcare Ltd. for an enterprise value of ₹1,600 crore. Plans include expanding its 376-bed Noida hospital to 480 beds by Q3FY26 and enhancing medical programs in key specialties.

- Lucknow Land Acquisition: Purchased 5.4 acres in Lucknow, with potential for a 550-bed hospital, strengthening its presence in high-growth markets.

- Dwarka Expansion: Opened a 303-bed Max Super Specialty Hospital in Dwarka under an asset-light model using management contracts and leases.

- Nagpur & Lucknow Mergers: Acquired Alexis Hospital (Nagpur) and Sahara Hospital (Lucknow), adding 750 beds. Lucknow is set to receive a 450-bed tower within 24 months.

- Capacity Growth: Plans to add 140 beds to both Lucknow and Nagpur hospitals, with further oncology department enhancements in Lucknow.

- Strategic Expansion: Focus on metro/tier-1 markets, leveraging acquisitions and asset-light models to scale operations efficiently.

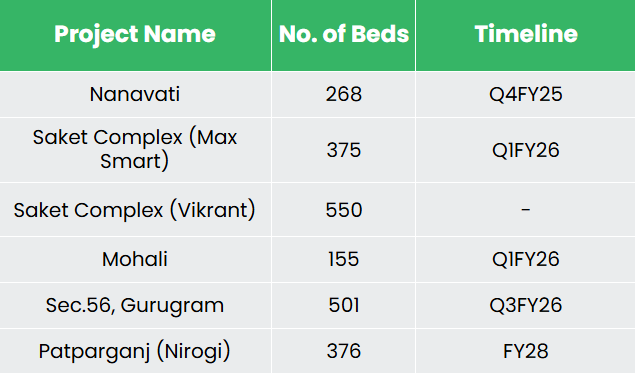

Capacity expansion projects:

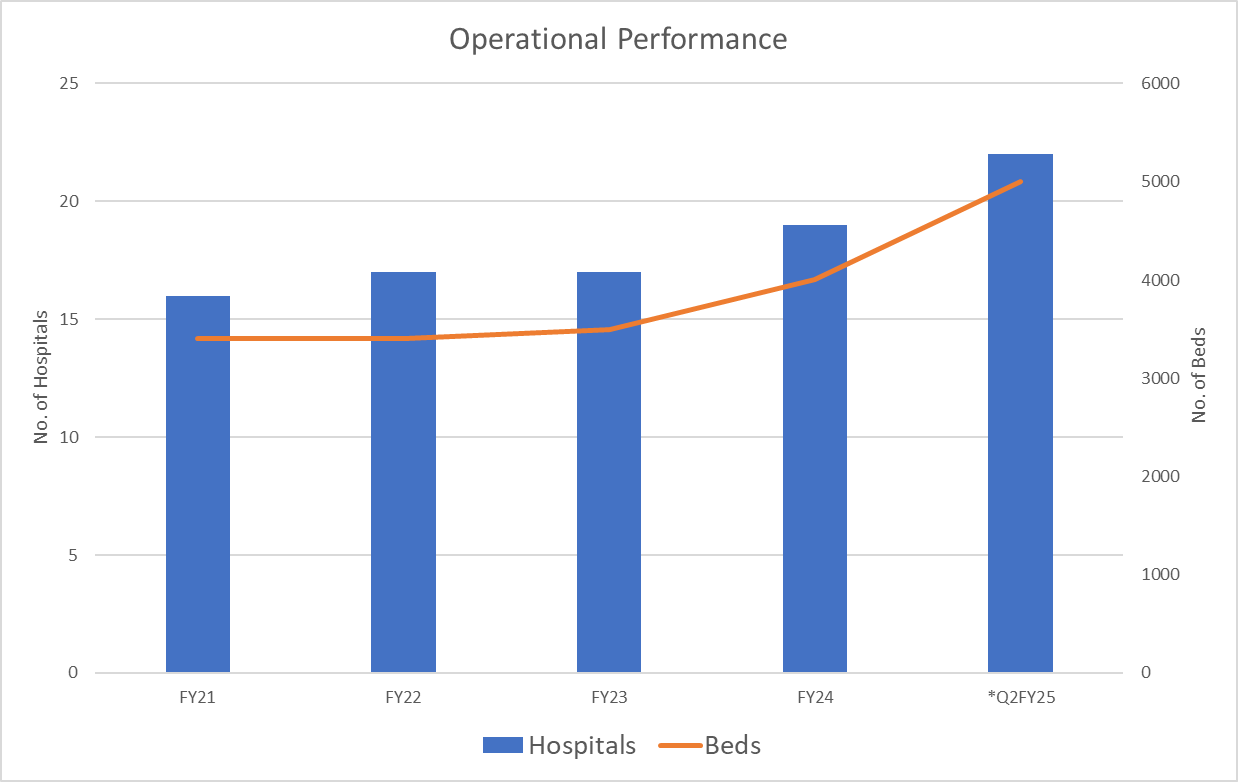

Operational Performance

Q2FY25

- Revenue Growth: Revenue rose 22% to ₹2,228 crore, up from ₹1,827 crore in Q2FY24.

- EBITDA Growth: EBITDA increased 14% to ₹566 crore, compared to ₹497 crore in Q2FY24.

- Net Profit Increase: Net profit grew 3% to ₹349 crore, compared to ₹338 crore in Q2FY24.

- Occupancy and OBD: Average occupancy stood at 77%, with Occupied Bed Days (OBD) up 18% YoY.

- ARPOB Growth: Average Revenue Per Operating Bed (ARPOB) rose 2% to ₹76,100.

- International Revenue: International patient revenue increased 12% YoY to ₹178 crore.

FY24

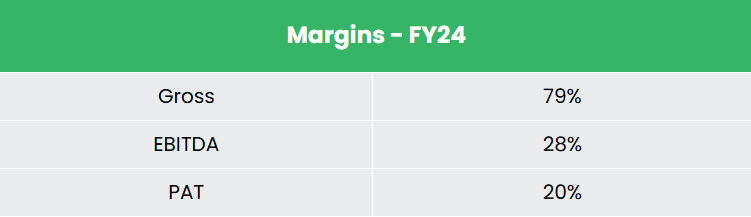

- Revenue Growth: Revenue grew 18% YoY to ₹5,406 crore in FY24.

- Operating Profit: Operating profit increased 20% YoY to ₹1,492 crore.

- Net Profit: Net profit stood at ₹1,058 crore, reflecting a 4% YoY decline.

- Capacity Expansion: Operationalized 122 additional beds at Max Hospital Shalimar Bagh during FY24.

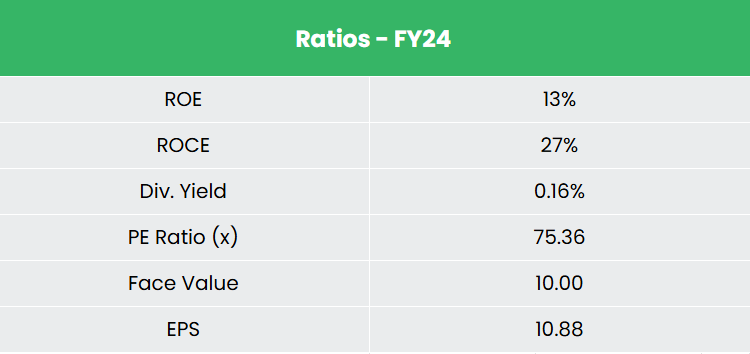

Financial Performance (FY21-24)

- Revenue & PAT Growth: 3-year CAGR of 29% (revenue) and 96% (PAT) between FY21-FY24.

- Profitability: Average ROE of 13% and ROCE of 14% over the past 3 years.

- Capital Structure: Strong financial health with a debt-to-equity ratio of 0.20.

Industry outlook

- Sector Growth: Healthcare is one of India’s largest sectors, driven by expanding coverage, improved services, and increased public-private spending.

- Hospital Market: Valued at $98.98 billion in 2023, it is projected to grow at a CAGR of 8.0%, reaching $193.59 billion by 2032.

- Key Drivers: Rising incomes, ageing population, growing health awareness, and a shift toward preventive healthcare are fueling demand.

- Competitive Edge: India benefits from a large pool of skilled medical professionals and cost advantages over Asian and Western peers.

Growth Drivers

- Skilled Workforce: India boasts a large pool of well-trained medical professionals.

- Increased Health Spending: Union Budget 2024-25 allocates ₹89,287 crore ($10.7 billion) to enhance healthcare accessibility and innovation.

- Infrastructure Boost: Government plans a ₹50,000 crore ($6.8 billion) credit incentive program to strengthen healthcare infrastructure.

Competitive Advantage

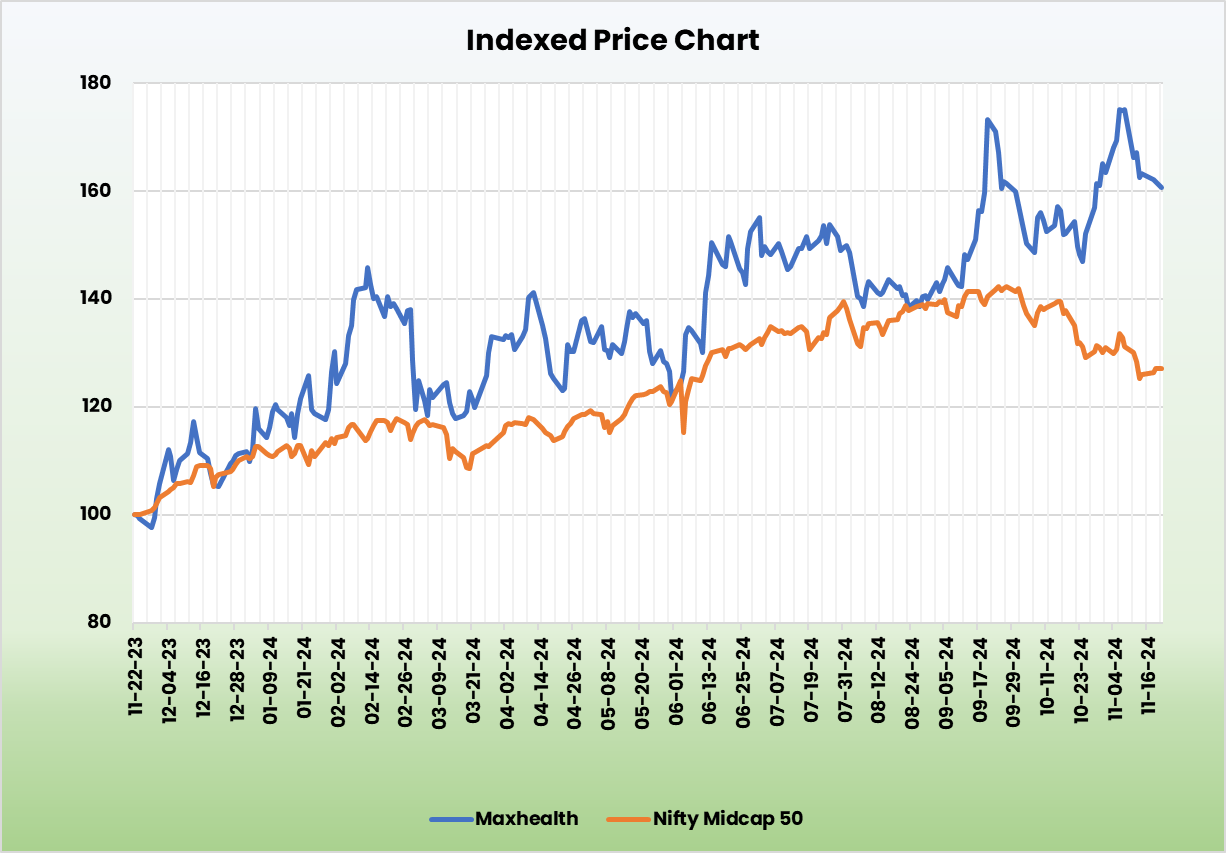

Max Healthcare stands out among competitors like Apollo Hospitals Enterprise Ltd and Fortis Healthcare Ltd by delivering steady sales growth and stable returns on invested capital, highlighting its operational efficiency and financial resilience.

Outlook

- Capacity Expansion: Plans to double its bed capacity from ~4,300 (FY24) within the next four years.

- Strategic Growth: Focused on brownfield and greenfield projects to enhance capacity at existing and new facilities.

- Metro-Centric Approach: Ensures access to skilled professionals and fosters opportunities in medical tourism.

- Regional Strengthening: Expanding presence in Lucknow and Nagpur as key growth markets.

- Nationwide Expansion: Targeting growth in Haryana, Maharashtra, Rajasthan, Punjab, Uttar Pradesh, and Madhya Pradesh.

Valuation

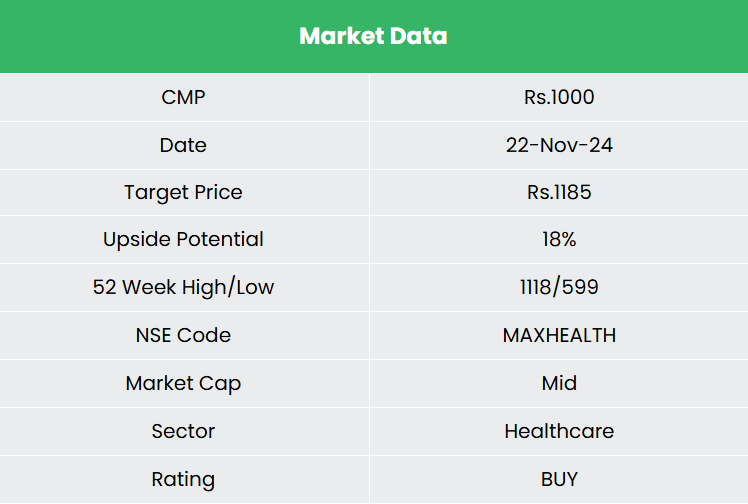

Max Healthcare’s strategies for consistent capacity expansions and penetration into newer geographies is expected to sustain its growth momentum. We recommend a BUY rating in the stock with the target price (TP) of Rs.1,185, 77x FY26E EPS.

Risks

- Regulatory Challenges: Exposure to varying laws and regulations across national and state jurisdictions may impact operations.

- Skilled Labour Shortage: Limited availability of skilled doctors and nursing staff might pose challenges to maintaining quality and supporting growth.

Note: Please note that this is not a recommendation and is intended only for educational purposes. So, kindly consult your financial advisor before investing.

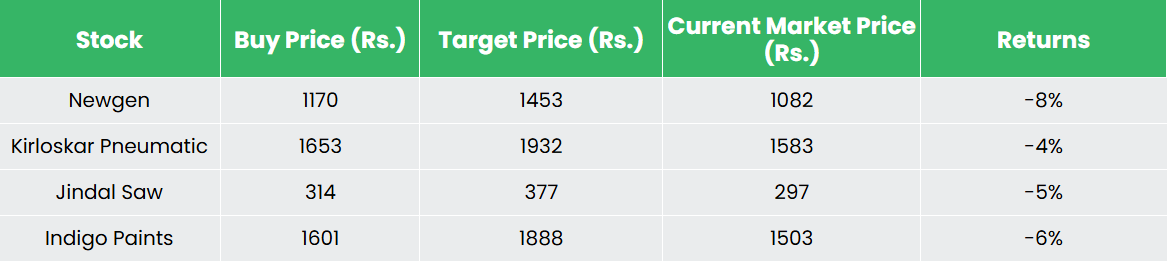

Recap of our previous recommendations (As on 22 November 2024)

Newgen Software Technologies Ltd

Kirloskar Pneumatic Company Ltd

Other articles you may like

Post Views:

119

{kind=link}