ASK Automotive Ltd – Driving safety through innovation

Founded in 1988, ASK Automotive Ltd. is a leading auto-ancillary company in India, specializing in advanced braking systems (ABS) for 2-wheelers and precision aluminium lightweighting solutions. A market leader in 2-wheeler ABS, including brake shoes and disc brake pads, ASK serves OEMs, OES, and IAM segments. With 17 manufacturing facilities across India, it exports to over 12 countries and employs 7,000+ people. The company partners with top brands like Honda, Hero MotoCorp, Suzuki, TVS, Yamaha, Bajaj, Royal Enfield, Ola, and Ather.

Products and Services

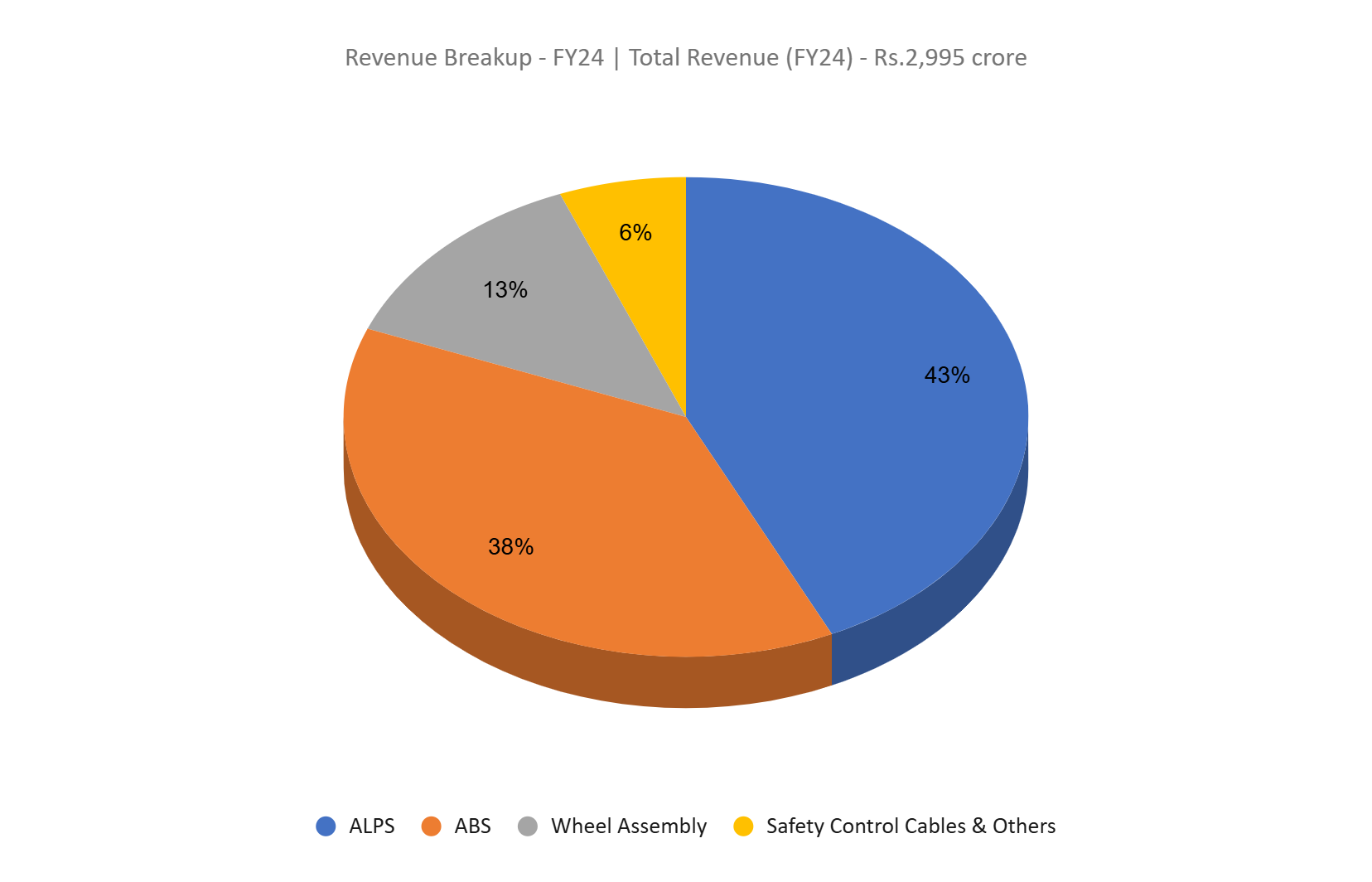

ASK Automotive Ltd. offers products across three key segments:

- Advanced Braking Systems (ABS):

Brake shoes, brake pads, brake panel assemblies, clutch plates, clutch shoes, brake linings, disc brake pads, and brake liners. - Aluminium Lightweight Precision Solutions (ALPS):

Crank cases, engine covers, pillion grips, ECU bodies, throttle bodies, and electric motor housings. - Safety Control Cables:

Front brake cables, rear brake cable assemblies, throttle cables, speedometer cable assemblies, and gear shift cables.

Subsidiaries: As of FY24, the company has 1 subsidiary and 1 joint venture.

Growth Strategies

- Market Leadership: Dominates India’s 2-wheeler ABS market with a ~50% share and is also a top manufacturer of ALPS and safety control cables, serving major OEMs with powertrain-agnostic products, including EV solutions.

- Expansion Plans: Setting up an 18th manufacturing plant in Bengaluru at an estimated cost of ₹200 crore, expected to be operational by Q4FY25 to cater to South India’s OEMs.

- Export Growth: Secured ₹75 crore in export orders during Q2FY25 and is focused on expanding its global footprint despite temporary disruptions in US operations.

- Renewable Energy Focus: Developing a 9.9 MWp mega solar power plant in Sirsa, Haryana, for in-house consumption, reinforcing its commitment to sustainability.

- EV Sector Push: Advancing lightweight aluminium products for EVs with a strong pipeline of innovative solutions tailored for EV OEMs.

- Diversification: Entering niche markets like 2-wheeler high-pressure die-cast (HPDC) alloy wheels to expand product offerings and market reach.

Financial Performance

Q2FY25

- Revenue Growth: Recorded ₹976 crore in revenue, a 22% YoY increase from ₹798 crore in Q2FY24.

- Segment Performance:

Advanced Braking Systems (ABS): Achieved 18% YoY growth, maintaining market leadership.

ALPS: Witnessed 27% YoY growth.

Safety Control Cables: Improved by 18% YoY.

- EBITDA Growth: Increased by 51% YoY to ₹119 crore from ₹79 crore, with EBITDA margin rising from 10% to 12%.

- Net Profit: Surged by 63% YoY to ₹67 crore compared to ₹41 crore in Q2FY24.

FY24

- Revenue Growth: Achieved ₹2,995 crore in revenue, marking a 17% YoY increase over FY23.

- Operating Profit: Recorded ₹311 crore, reflecting a 25% YoY growth.

- Net Profit: Posted ₹174 crore, a significant 41% YoY increase.

- Expansion: Successfully commenced operations at a new manufacturing plant in Karoli, Rajasthan.

Financial Performance (FY21-24)

- Revenue & PAT Growth: The company has achieved a revenue and PAT CAGR of 25% and 23%, respectively, over the 3-year period from FY21-24.

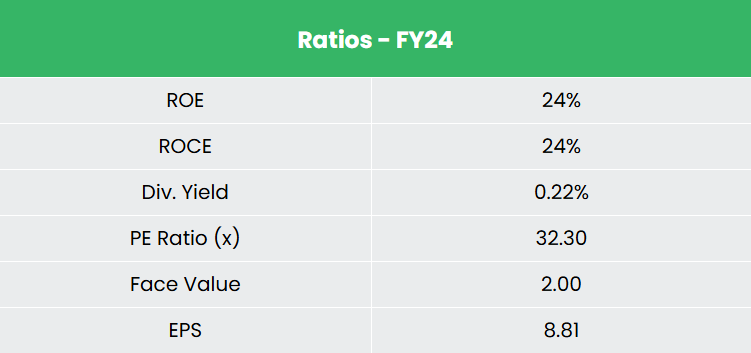

- Strong Return Ratios: Average ROE and ROCE stand at 19% and 20%, respectively, for the FY21-24 period.

- Capital Structure: The company maintains a strong capital structure with a debt-to-equity ratio of 0.43.

Industry outlook

- Rising Demand: India’s auto components industry has grown significantly, driven by increasing incomes, infrastructure investments, and manufacturing incentives.

- Two-Wheeler Segment Dominance: The two-wheeler market, propelled by a growing middle class, led the industry with 23.85 million units sold in FY24.

- OEM Growth: The surge in automobile demand has fueled the growth of original equipment manufacturers (OEMs) and auto component producers.

- Global Appeal: India’s automotive manufacturing expertise has boosted international demand for its vehicles and components.

- Localization Boost: The increasing presence of global OEMs in India has accelerated the localization of their components.

Growth Drivers

- Demographic Advantage: Expansion of the working population and a growing middle class are fueling demand.

- FDI Support: 100% FDI under the automatic route boosts investments in the auto components sector.

- Future Potential: The Indian auto components industry is projected to reach US$ 200 billion by FY26, highlighting robust growth opportunities.

Competitive Advantage

ASK Automotive stands out among competitors like Endurance Technologies Ltd. and Uno Minda Ltd., showcasing steady revenue growth, superior return ratios, and robust earnings potential. Its financial stability and efficient capital utilization underline its ability to deliver consistent income and returns, setting it apart in the auto components industry.

Outlook

- Karoli Plant Ramp-Up: Production at the new facility has achieved positive EBITDA margins, with full capacity utilization expected in 1-2 years.

- Investment Plans: CAPEX guidance set at ₹250-300 crore for FY25, alongside a targeted 25% ROE.

- Growth Drivers: Expansion supported by economies of scale, new orders, client acquisitions, increased production at new facilities, and cost optimization efforts.

- Sustainability Commitment: The nearing completion of a solar plant aligns with sustainability goals, offering a 5-year payback period.

- Debt Reduction: Actively working on lowering the debt ratio to strengthen the capital structure.

- Recognition: A recent rating upgrade from CRISIL underscores the company’s robust business model and growth potential.

Valuation

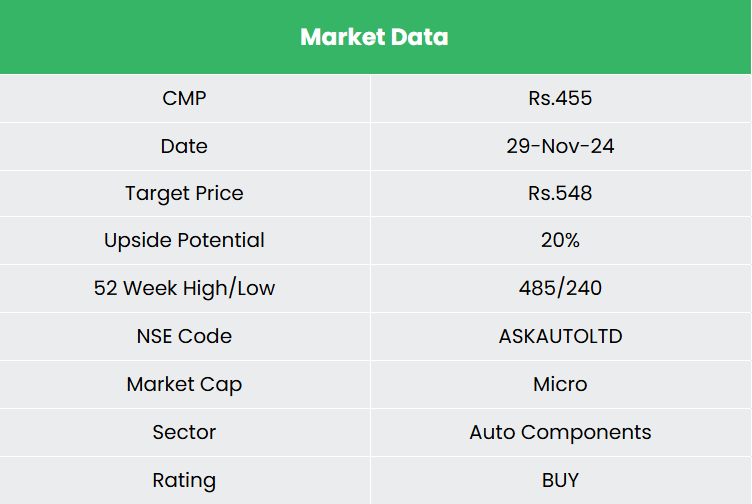

ASK Automotive’s market leadership, strategic focus on the EV sector, export expansion, and product diversification position it for sustained growth. These factors drive our positive outlook, leading to a BUY recommendation with a target price (TP) of ₹548, representing 47x FY26E EPS.

Risks

- Industry Risk: Approximately 80% of the company’s revenue comes from India’s 2-wheeler automotive sector. Any adverse changes in this industry could negatively affect the company’s operations and financial health.

- Raw Material Price Volatility: Disruptions in the supply or fluctuations in the prices of key materials, particularly aluminium, could put pressure on the company’s margins.

Note: Please note that this is not a recommendation and is intended only for educational purposes. So, kindly consult your financial advisor before investing.

Recap of our previous recommendations (As on 29 November 2024)

Newgen Software Technologies Ltd

Kirloskar Pneumatic Company Ltd

Other articles you may like

Post Views:

162

{kind=link}