BLS International Services Ltd – Beyond Boundaries

Founded in 1983 and headquartered in New Delhi, BLS International Services Ltd. is a global leader in outsourcing and technology solutions. It provides visa, passport, consular, biometric, attestation, and citizen services to governments and diplomatic missions worldwide. With operations in 66+ countries, serving 46+ client governments, it is the world’s second-largest player. The company also offers digital services like Business Correspondent (BC) solutions, e-governance, and assisted e-services in India.

Products and Services

BLS International offers a wide range of services, including:

- Visa Processing: e-visas, visa applications, and biometrics.

- Citizen Services: Passport applications, national identity cards, and travel documents.

- Digital Services: E-governance, business correspondent services, and banking-related services for account holders.

- Verification and Attestation: Document verification, notarial cards, and attestation services.

- Value-Added Services: Courier services, domestic money transfers, Aadhaar card services, and IT solutions.

Subsidiaries – As of FY24, the company has 27 subsidiaries.

Growth Strategies

- Established Market Leader: BLS International is a top global player in visa and consular (VC) services, e-governance, and digital solutions, serving governments and consulates in countries like Slovakia, Hungary, Italy, Poland, and Portugal, with over 121,000 digital service touchpoints across urban and rural areas.

- Diverse Offerings: The company delivers G2C services in sectors like food, health, revenue, education, and social justice, alongside B2C services, enhancing access in underserved regions.

- Strategic Acquisitions: Recent acquisitions include iDATA (Turkey), Citizenship Invest (Dubai), and SLW Media (sports management), expanding its global reach, improving margins, and creating unique synergies like combining sports events with visa services.

- Scaling Operations: Transitioning from partner-managed to self-managed centers has improved margins, while its definitive agreement to acquire Aadifidelis Solutions strengthens its position in India’s loan processing sector.

- Impressive Financials: iDATA, with operations in 15+ countries, reported Q2FY25 revenue of ₹60 crore and a 37% EBITDA margin, while Citizenship Invest enhances services for high-net-worth individuals in residency and citizenship programs.

Operational Performance

Q2FY25

- Revenue Growth: Achieved ₹495 crore in revenue, a 21% increase from ₹408 crore in Q2FY24.

- EBITDA Surge: EBITDA grew 89% YoY to ₹164 crore, with margins improving by 1,186 bps to 33%.

- Net Profit: Net profit rose 78% YoY to ₹146 crore, with margins improving by 933 bps to 29%.

- Strong Balance Sheet: Maintained a robust net cash balance of ₹902 crore.

- Expansion: Opened new visa application centers in Colombia and Peru, strengthening global presence.

FY24

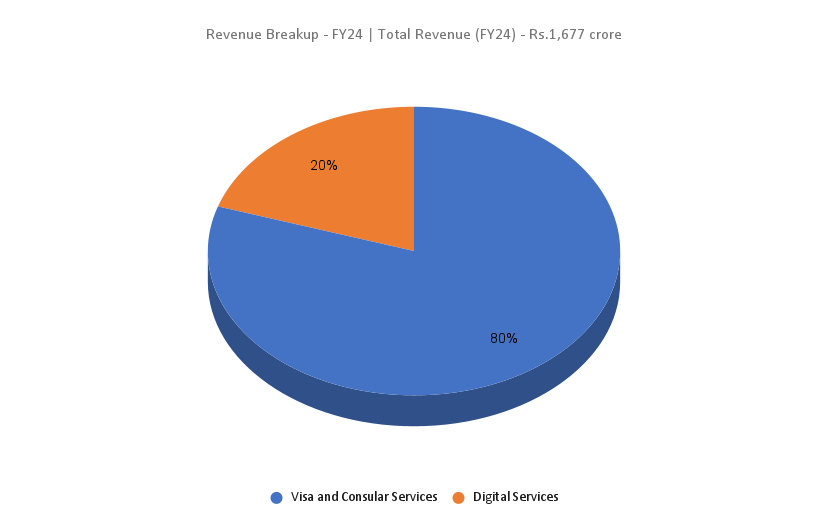

- Revenue Growth: Recorded ₹1,677 crore in revenue, up 11% YoY.

- Operating Profit: Achieved ₹346 crore, a 57% YoY increase.

- Net Profit: Posted ₹326 crore, a significant 60% YoY growth.

- Subsidiary IPO: Successfully raised ₹300 crore through the IPO of BLS E-Services Limited, boosting growth and expansion plans.

Financial Performance (FY21-24)

- 3-Year CAGR (FY21-24): Revenue grew at 52%, while net profit grew at 84%.

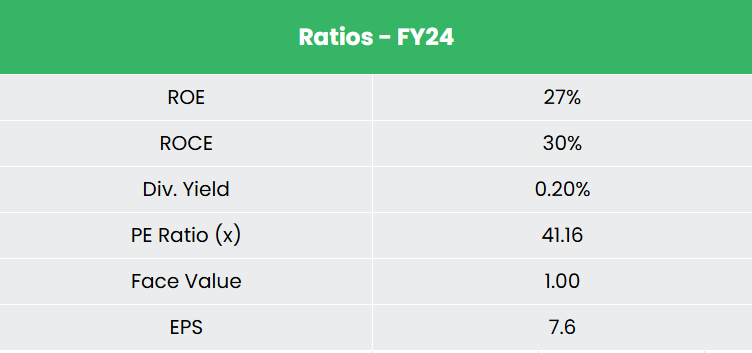

- Profitability Metrics: Average 3-year ROE and ROCE stood at 28% each.

- Strong Capital Structure: The company maintains a healthy debt-to-equity ratio of 0.27.

Industry outlook

- Key Role: Visa and consular outsourcing simplifies applications for various visa types, including business, work, study, and tourism visas.

- Efficiency: Third-party companies enhance efficiency and improve customer experience through streamlined processes.

- Market Growth: The global visa outsourcing market is expected to grow at a 14% CAGR, expanding from USD 3.7 billion in 2023 to USD 8.3 billion by 2028.

- Driving Factors: Growth is fueled by increasing visa demand and advancements in service offerings.

Growth Drivers

- E-Governance Expansion: Initiatives like Digital India, Aadhaar, online tax filing, and digital land management systems are driving demand for digital services and e-governance solutions.

- Focus on Financial Inclusion: Government and banking sector emphasis on financial inclusion is creating opportunities in digital and assisted services across urban and rural areas.

- Tourism Growth: Rising interest in various forms of tourism—cultural, wellness, adventure, and coastal—is fueling demand for efficient visa processing and consular services globally.

Competitive Advantage

BLS is the only listed player in India in the visa and consular space. Being a monopoly in its segment, we have compared the company with other listed IT-Software companies. BLS is generating higher returns from the invested capital indicating the company’s prudent capital allocation strategies.

Outlook

- Enhanced Margins: Transitioning from partner-run to self-run centers and synergies from strategic acquisitions are expected to boost margin profiles significantly.

- Revenue Growth Guidance: The company anticipates consolidated revenue growth of 22-23% and iDATA revenue growth of 10-15% for FY25, supported by higher service charges from key acquisitions.

- Contract Wins and Renewals: Success in winning new contracts and renewing existing ones, with increased service fees in some cases, is expected to drive sustained profitability.

Valuation

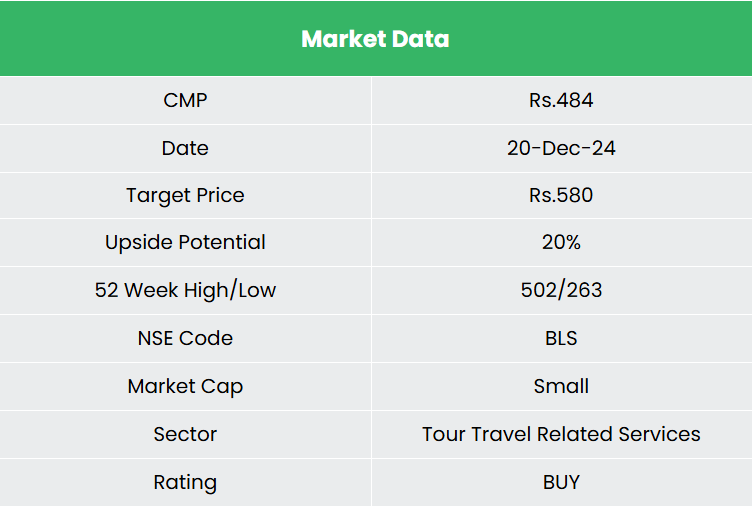

We anticipate that BLS International will sustain its growth momentum as an established global leader in an oligopolistic market. We recommend a BUY rating with a target price (TP) of ₹580, based on a 40x FY26E EPS.

Risks

- Forex Risk: With significant operations in foreign markets, BLS is exposed to forex risk. Unforeseen fluctuations in currency exchange rates could negatively impact the company.

- Geopolitical Risk: Geopolitical tensions, diplomatic disputes, or changes in immigration policies may restrict cross-border movement, affecting the company’s operations.

Note: Please note that this is not a recommendation and is intended only for educational purposes. So, kindly consult your financial advisor before investing.

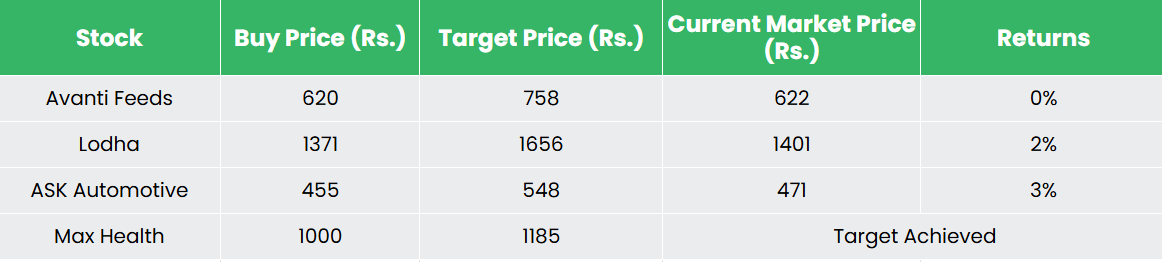

Recap of our previous recommendations (As on 20 December 2024)

Other articles you may like

Post Views:

144

{kind=link}