TVS Motor Company Ltd – Shaping Tomorrow’s Mobility Today

Incorporated in 1992 and headquartered in Chennai, TVS Motor Company Ltd (TVSM) is a globally recognized manufacturer of two and three wheelers (2 & 3W). The company has presence in 80+ countries across Middle East, Africa, SE Asia, Indian Subcontinent, Latin and Central America. Backed by 5 manufacturing facilities in India (located in Hosur, Mysuru and Nalagarh) and one each in Indonesia & UK, the company is currently the third largest 2W manufacturer in India and fourth largest in the world. The company is also in the business of financing of two wheelers, used cars, used and new tractors, used commercial vehicles, consumer durables, digital finance products, emerging and corporate business loans and personal loans via its retail finance arm TVS Credit Services.

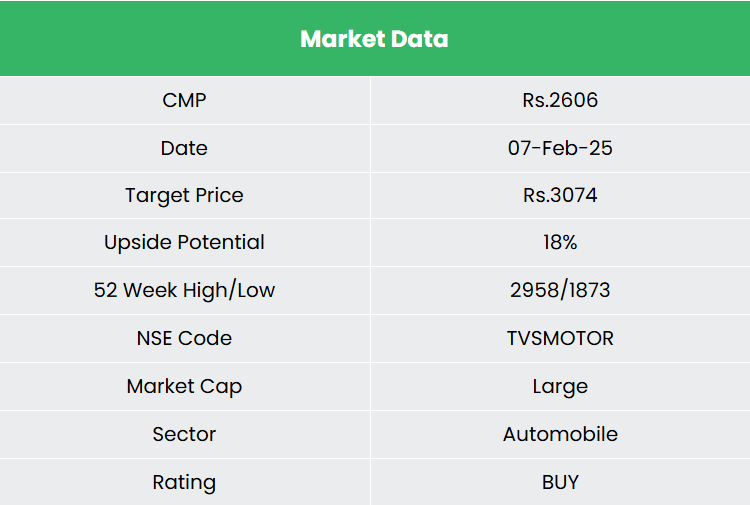

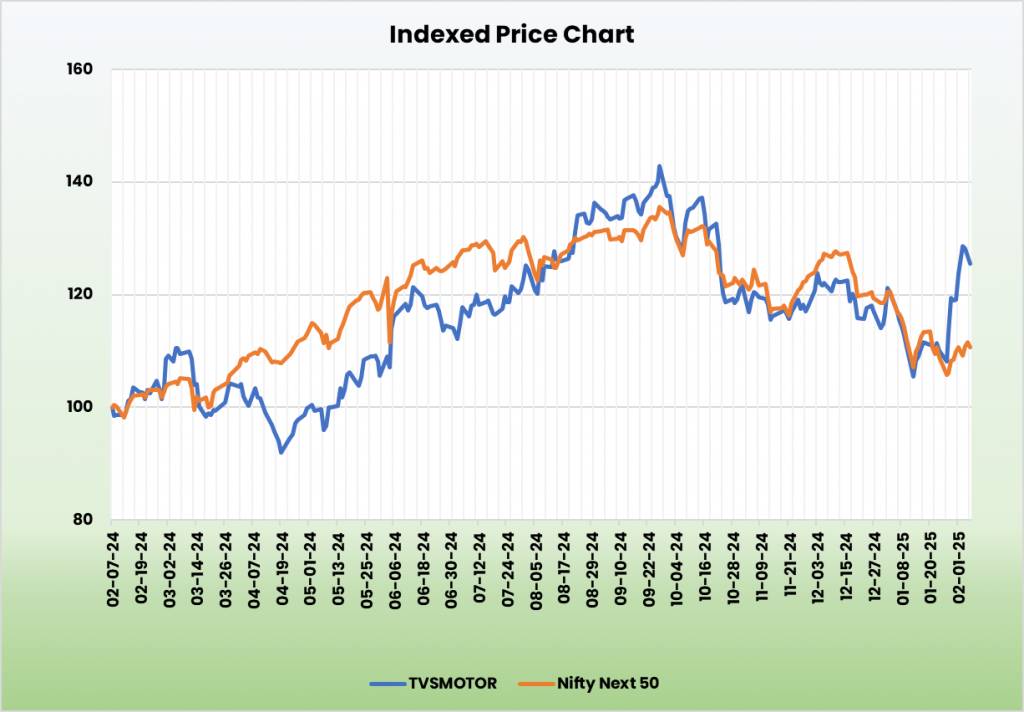

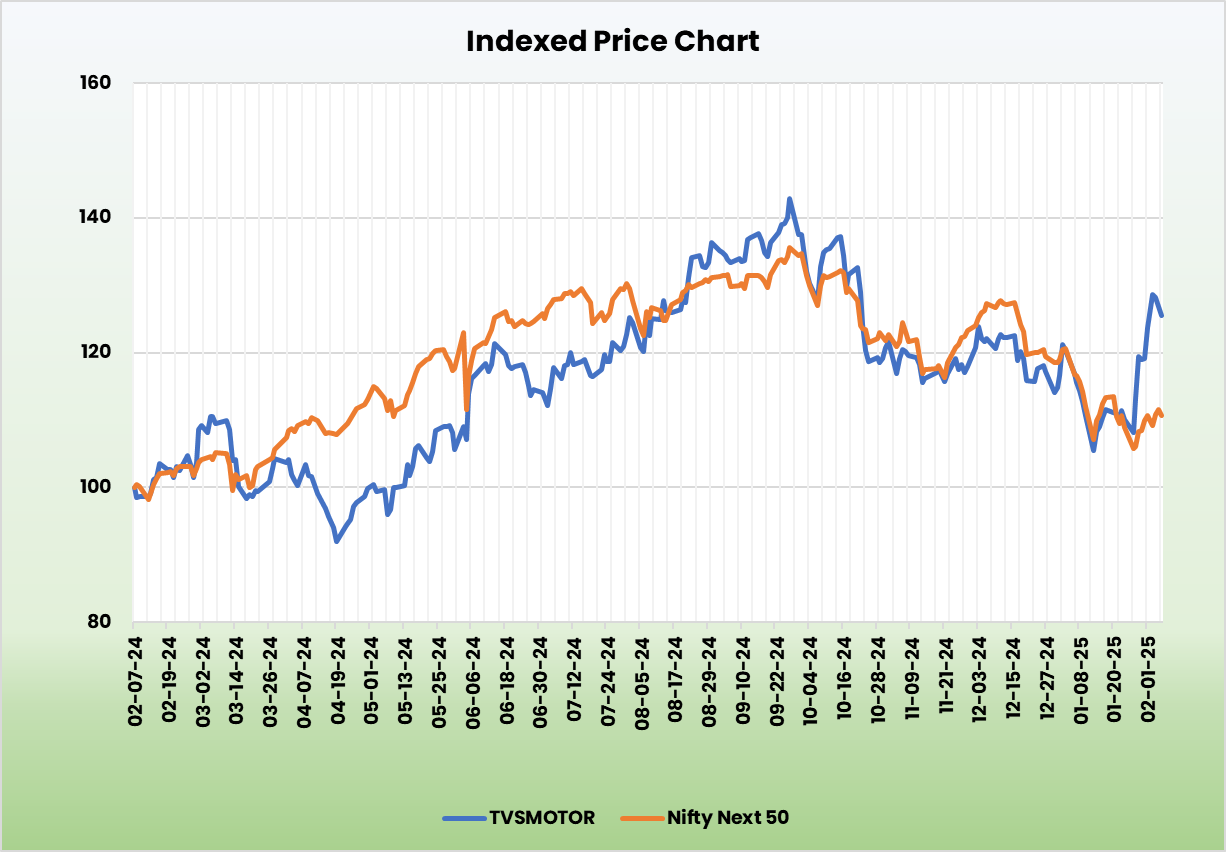

We rate TVSMOTOR a ‘BUY’ as it has strong growth prospects as a 2-wheeler manufacturer and fundamentals to be considered as FundsIndia’s Alpha Stock Pick.

Products and Services

Products offered by the company includes motorcycles & scooters (including electric 2W), 3 wheelers (including electric 3W), mopeds. It is also in the business of providing finance via its retail finance arm TVS Credit Services.

Subsidiaries: As of FY24, the company has 16 subsidiaries and 11 associate companies.

Investment Rationale

- New product launches – The company continues to expand its portfolio with new products and variants. In Q3FY25, it introduced the fastest 125cc motorcycle in the segment, the TVS Raider iGO Variant, along with the TVS Apache RTR 160 4V featuring upside-down suspension (USD). A significant milestone was the launch of the company’s first electric 3W, the TVS King EV MAX, during the same quarter. Initially available at select dealerships, the company plans to expand sales in the next two quarters. The TVS Jupiter 110, launched in Q2FY25, has been well-received in the market. Additionally, the company launched several new products in FY24, including the TVS X, TVS Raider SS Edition, TVS iQUBE, TVS Apache RTR 310, TVS HLX 150F, TVS Ronin, and TVS NEO AMI 125. This timely expansion of product portfolio is expected to benefit the company in terms of market differentiation and competitive edge as well as building customer loyalty and retention.

- Diversified operations – The company offers a wide variety of products, ranging from 2W to 3W models in both ICE (Internal Combustion Engine) and EV variants. The company’s offerings span across affordable 2W & 3W to racing-inspired bikes. In the latest quarter, domestic sales of 2W ICE grew by 5% year-over-year, outperforming the industry’s 1% growth. International sales of 2W ICE saw a notable 26% increase. Additionally, EV 2W sales surged by 57% during the period. TVS Credit added over 3 million new customers this year, bringing its total customer base to over 17.7 million. The book size expanded by 7%, reaching Rs.27,190 crore, while profit before tax rose by 40%, reaching Rs.321 crore.

- Q3FY25 – The company generated standalone revenue of Rs.9,097 crore, which is an increase of 10% compared to Q3FY24. EBITDA grew by 17% YoY to Rs.1,081 crore. The company reported net profit of Rs.618 crore which is an increase of 4% compared to the corresponding quarter of the previous year.

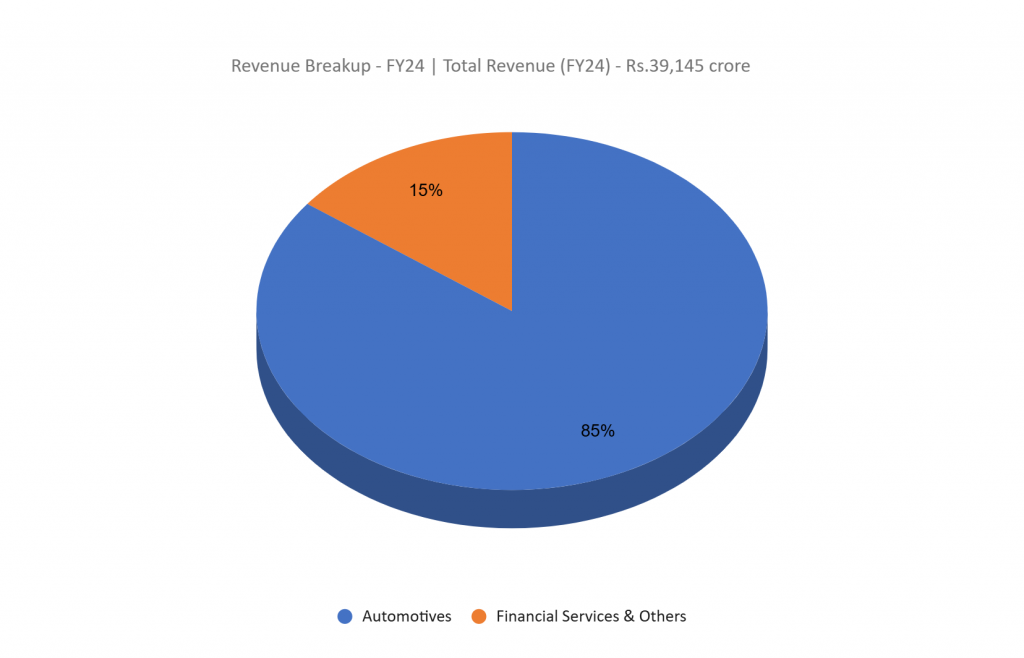

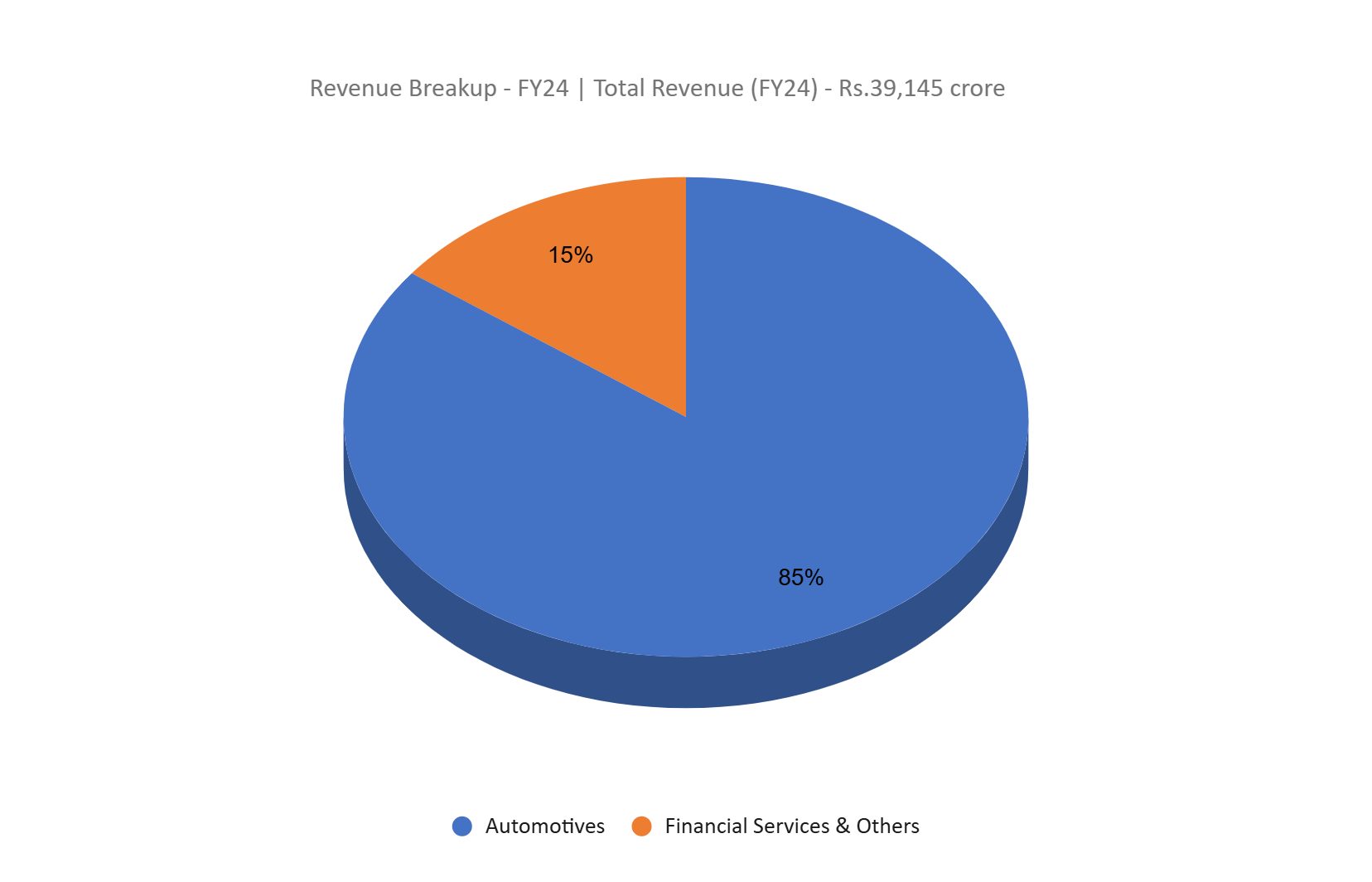

- FY24 – The company generated revenue of Rs.39,145 crore, an increase of 22% compared to FY23 revenue. Operating profit is at Rs.5,500 crore, up by 37% YoY. The company posted net profit of Rs.1,779 crore, a jump of 36% YoY. During the period the company surpassed 4 million two-wheeler sales for the first time. The company’s domestic ICE 2W volume increased by 19% against the industry growth of 13%. EV volume doubled from 97,000 of last year to 194,000. In the international markets, 2W sales grew by 47% to 2.36 lakhs.

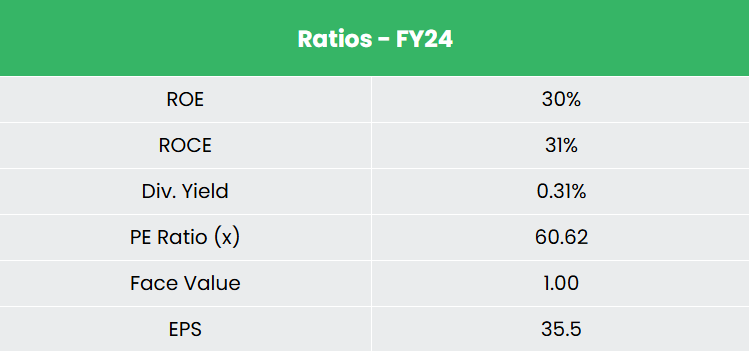

- Financial Performance – The company has generated a revenue and PAT CAGR of 26% and 39% over the period of 3 years (FY21-24). Average 3-year ROE & ROCE is around 24% and 13% for FY21-24 period.

Industry

The Indian automobile industry has traditionally been a strong indicator of the country’s economic health, as it plays a pivotal role in driving both macroeconomic growth and technological progress. The two-wheeler segment leads the market in terms of volume, fuelled by a growing middle class and a large, youthful population. Additionally, the increasing interest of companies in tapping into rural markets has further supported the sector’s growth. On a global scale, the electric vehicle (EV) market was valued at around US$ 250 billion in 2021 and is expected to expand fivefold to US$ 1,318 billion by 2028. By 2030, the Indian government has set a target for 30% of new vehicle sales in the country to be electric.

Growth Drivers

- The Centre has launched the PM E-DRIVE scheme with a budget of US$ 1.30 billion (Rs. 10,900 crore), effective from October 1, 2024, to March 31, 2026. The initiative aims to accelerate the adoption of Electric Vehicles (EVs), establish charging infrastructure, and develop an EV manufacturing ecosystem in India.

- The Government of India encourages foreign investment in the automobile sector and has allowed 100% FDI under the automatic route.

- The reduction in the tax burden in the 2025-26 Union Budget is expected to boost spending among the expanding middle class population.

Peer Analysis

Competitors: Hero MotoCorp Ltd, Bajaj Auto Ltd, etc.

The company is generating stable return ratios in line with the growth in the sales. This indicates the company’s ability to generate better profits for the capital invested.

Outlook

The company boasts a strong R&D team that is crucial in understanding evolving customer needs and market trends. This enables the company to proactively introduce successful products and capture market share. For FY25, the company has set a capital expenditure guidance of Rs.1,700 crore, with a significant portion dedicated to product development. It remains committed to growing its presence in international markets, focusing on regions like Africa and Latin America, and has recently entered Morocco. This strategy of continuous innovation, diverse product offerings, and market adaptability ensures the company stays competitive, expands its customer base, and keeps pace with market shifts. It is also anticipating the start of Production Linked Incentive (PLI) benefits from Q4FY25, which should support margin growth.

Valuation

We expect the company to sustain its market share gains led by aggressive product pipeline and strong execution capabilities. We recommend a BUY rating in the stock with the target price (TP) of Rs. 3,074, 49x FY26E EPS.

Risk

- Credit risk – The company has high proportion of debt in its capital structure, which may impact its profitability, cash reserves, and capacity to raise further capital.

- Macro-economic conditions – Changes in macro-economic conditions such as high inflation, economic slowdown, high interest rates etc. could have an adverse impact on the company turnover.

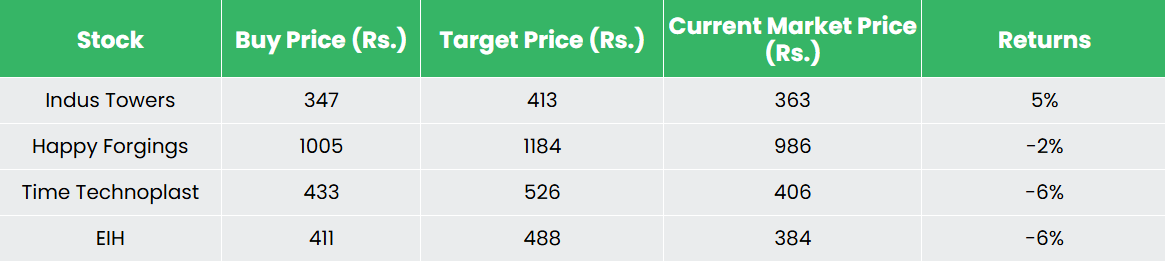

Recap of our previous recommendations (As on 07 February 2025)

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.

Other articles you may like

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}