Interglobe Aviation Ltd – Giving wings to the nation

Incorporated in 2004 and headquartered in Gurugram, Interglobe Aviation Ltd. is India’s largest passenger airline and amongst the fastest growing airlines in the world. It is in the low-cost carrier (LCC) segment of airline industry in India. With a fleet of over 400 aircrafts, the company runs more than 2,200 daily flights, serving over 125 destinations, including 38 international ones. It has also partnered with 10 airlines for codeshare agreements. The airline covers 552 routes both domestically and internationally. On the global stage, it ranks 7th for daily flights and 5th for passengers carried.

Products and Services

The company derives its income predominantly from passenger ticket revenue, revenue from ancillary products and services such as cargo, excess baggage, special service requests, ticket modification and cancellation, in-flight sales and tours.

Subsidiaries: As of FY24, the company has 2 subsidiaries and no associate companies/joint ventures.

Investment Rationale

- Expansion plans – In just 18 years, IndiGo has become the seventh-largest airline in the world by daily departures and the first Indian airline to operate a fleet of over 350 aircraft. It also became the youngest airline globally to serve 100 million customers in a single year. It has placed an order for 500 A320 neo family aircraft, the largest single order ever made by any airline with Airbus, along with 30 A350-900 aircrafts. This brings its order book to 1,000 aircraft, set for delivery by 2035. The company has also planned to expand its capacity through wet leases. During FY25, it signed codeshare agreement with British Airways and a MUA for codeshare partnership with Malaysian Airlines.

- Growth strategies – The company had launched new business class – Indigo Stretch on the Delhi-Mumbai route. It is expanding the routes to Delhi-Bengaluru and Delhi-Chennai route in the short-term supported by a long-term plan to expand to 12 routes with a fleet of 40+ aircrafts by the end of FY25. Its loyalty program Bluechip (to be launched in October) is expected to aid in customer retention. The company is taking significant steps towards limiting its forex volatility in its financial statements by hedging part of its foreign currency outflows.

- Q3FY25 – The company generated a revenue of Rs.22,111 crore, achieving an increase of 14% as compared to the Rs.19,452 crore of Q3FY24. EBITDA improved by 11% YoY, from Rs.5,475 crore to Rs.6,059 crore. The company welcomed 31 million passengers, the highest ever in any quarter. Profitability was impacted due to the rupee depreciation during the period, resulting in a higher unrealised exchange loss of around Rs.1,400 crore during the period. Net profit saw a decline of 18% from Rs.2,998 crore of Q3FY24 to Rs.2,449 crore of the current quarter. It generated free cash of Rs.28,900 crore, and additional Rs.14,000 crore in restricted cash.

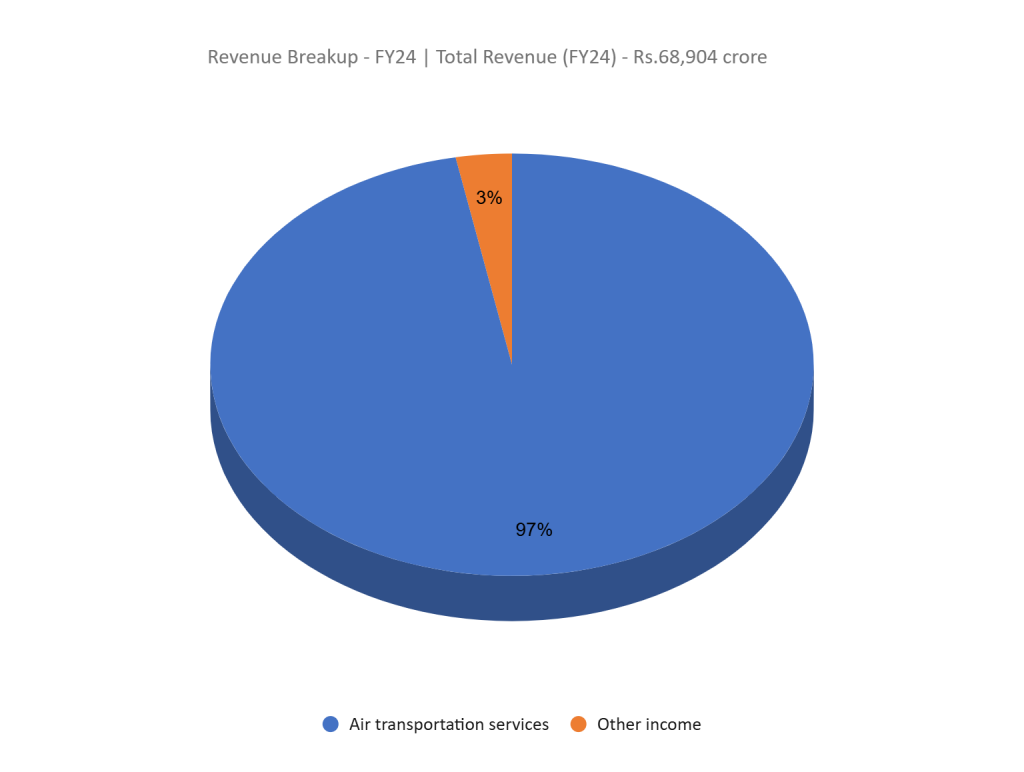

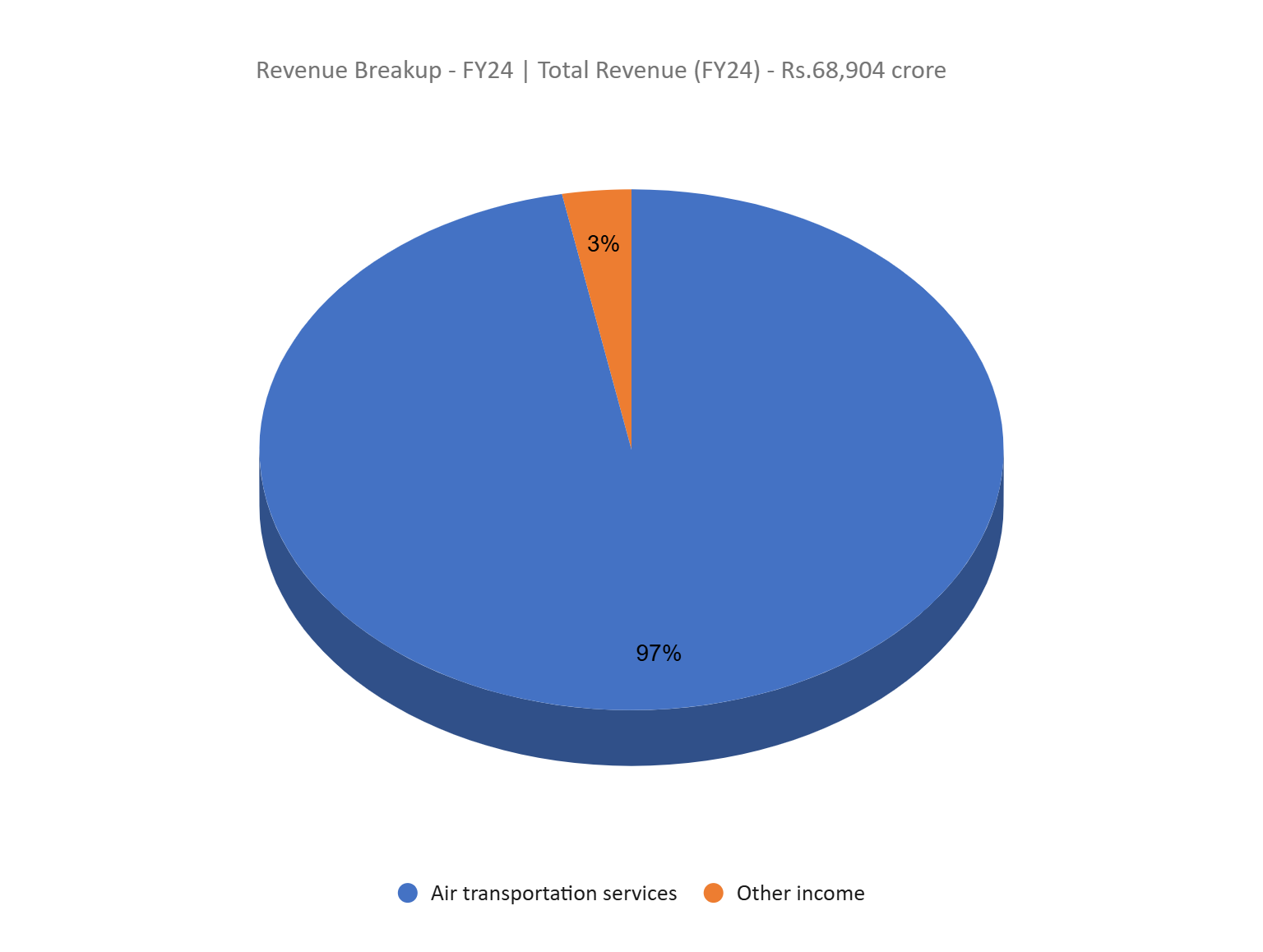

- FY24 – The company generated revenue of Rs.68,904 crore, an increase of 27% compared to FY23 revenue. Operating profit is at Rs.17,545 crore, up by 140% YoY. The company posted net profit of Rs.8,172 crore against a loss reported for FY23. During the FY the company added 65 aircrafts including 12 damp-leased aircrafts. Revenue per available seat kilometre (RASK) increased by 3.2% from Rs.4.80 in FY23 to Rs.4.96 in FY24, driven by increase in yields and passenger load. Cost per Available Seat kilometer (CASK) decreased by 9.3% from Rs.4.83 in FY23 to Rs.4.38 in FY24.

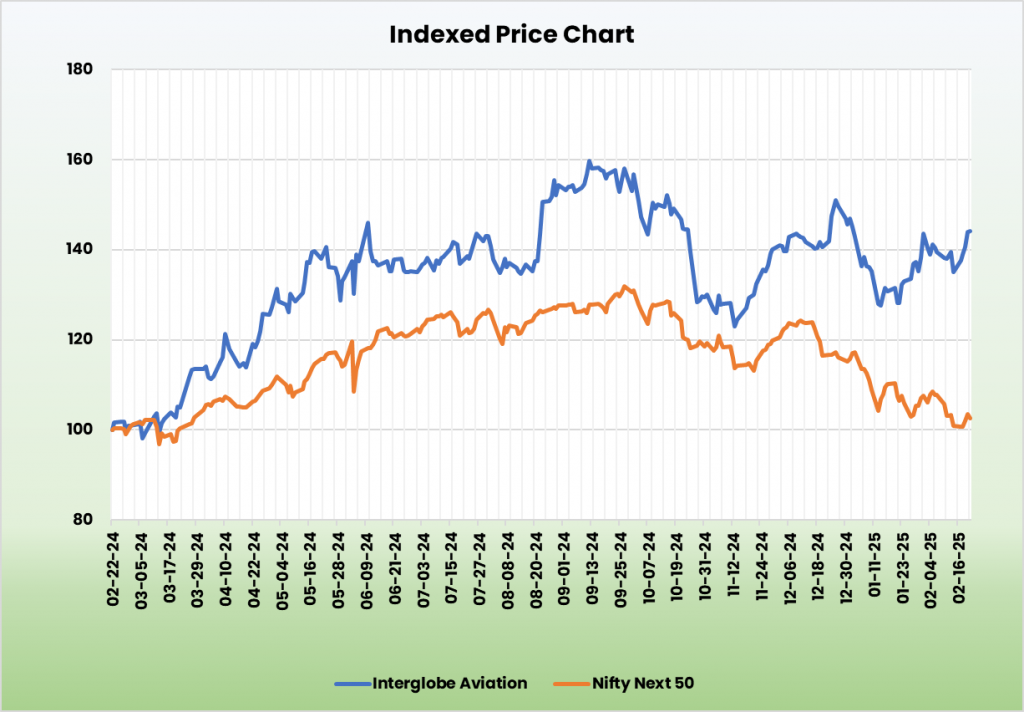

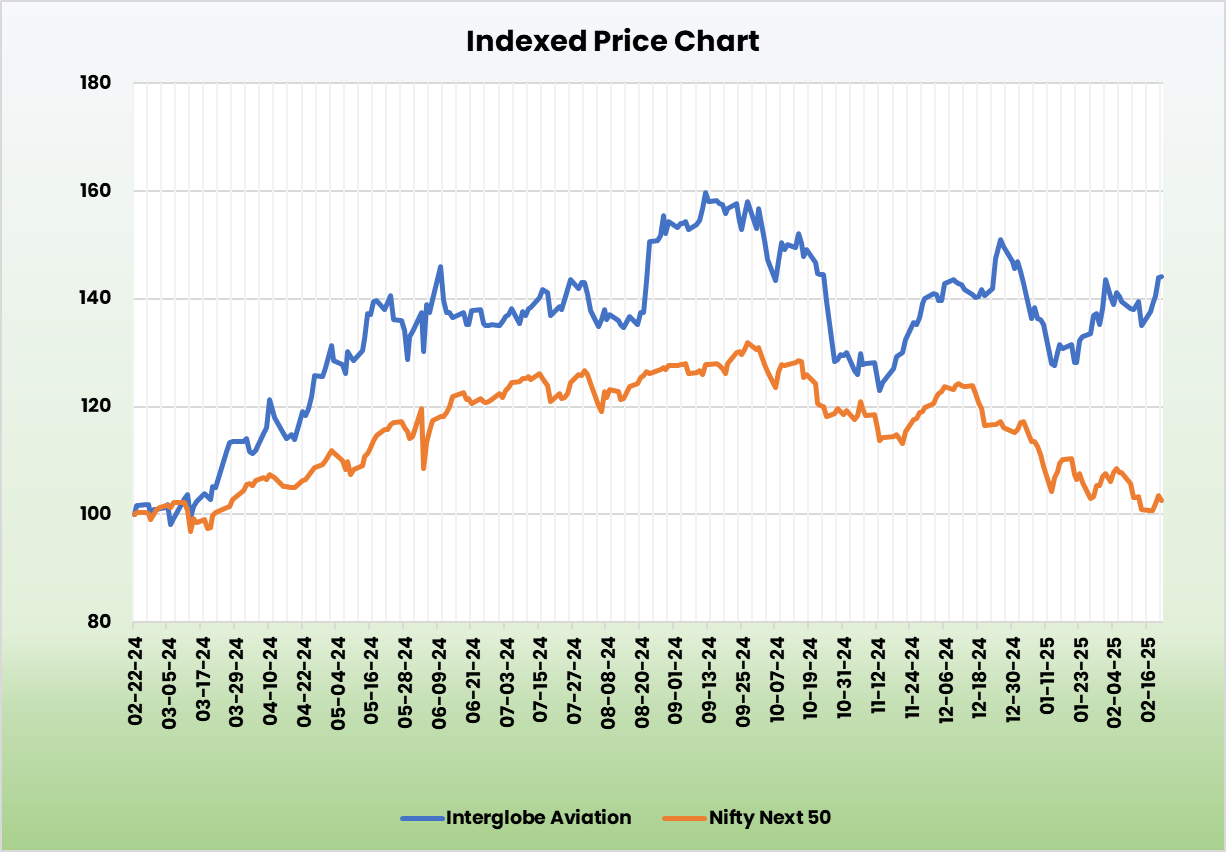

- Financial and operational performance – The company has achieved a 68% revenue and 47% net profit CAGR over the past 3 years (FY21-24). While its debt is higher due to leased airlines, its debt-to-equity ratio stood at ~26.00 in FY24, and 0.95 excluding lease liabilities. Operationally, it added 50 new routes in Q3FY25, maintained an 87% load factor (% of available seats that are filled by passengers).

Industry

India’s aviation industry, largely untapped and full of growth opportunities, is set to see a significant rise in demand due to the expanding middle-class demographic and increasing industrialization. With nearly 40% of the population being upwardly mobile middle-class, air travel remains expensive for the majority, but government policies and initiatives are aimed at making it more affordable and accessible. As the economy grows and people and freight movements increase, demand for air travel is rising rapidly, positioning India as a potential global aviation hub, with projections to reach 300 million domestic passengers by 2030. The government’s Regional Connectivity Scheme, ‘UDAN,’ aims to connect Tier-2 and Tier-3 cities with major hubs through subsidized fares and infrastructure development, unlocking the sector’s full potential.

Growth Drivers

- As per the present FDI Policy, 100% FDI is permitted in scheduled Air Transport Service/Domestic Scheduled Passenger Airline (Automatic upto 49% and Government route beyond 49%). However, for NRIs 100% FDI is permitted under automatic route in Scheduled Air Transport Service/Domestic Scheduled Passenger Airline.

- The Ministry of Civil Aviation was given an allocation of Rs.2,357 crore (US$ 282 million) in the budget for 2024-25.

- Estimated increase in the tourism sector following the reduction in the tax burden in the 2025-26 Union Budget is expected to boost spending among the expanding middle class population

Peer Analysis

Competitor: SpiceJet Ltd

Indigo is currently the only profit-generating listed airline in the nation, solidifying its dominant position in the industry.

Outlook

In Q3FY25, the company faced a forex impact due to a significant portion of its lease and maintenance liabilities being denominated in US dollars. To mitigate this, the management has devised a strategy to hedge 60-70% of its positions over the next 12 months, using a combination of natural hedging and forward instruments. Expanding international routes, which will increase foreign revenue, is expected to serve as a natural hedge against these costs. Currently holding a 28% share in international markets, the company aims to grow this to 30% by FY25. It has provided a capacity growth guidance of 10-12% for FY25, with a 20% YoY increase in capacity for Q4FY25. Additionally, it aims to reduce AOG (Aircraft on Ground) to the mid-40s by the start of FY26.

Valuation

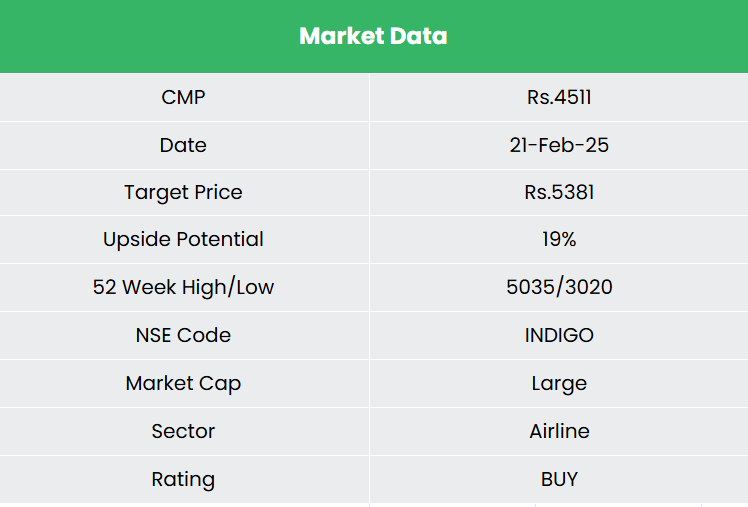

Given the untapped potential of air travel in the country, combined with the company’s strong position in the industry, we believe it is well placed to reach new heights. We recommend a BUY rating in the stock with the target price (TP) of Rs.5,381, 23x FY26E EPS.

Risk

- Forex risk – The company has significant operations in foreign markets and hence is exposed to forex risk. Any unforeseen movement in the forex market can adversely affect the company.

- Input cost variance – The margins are prone to take a dip if there is a surge in input costs – predominantly fuel cost.

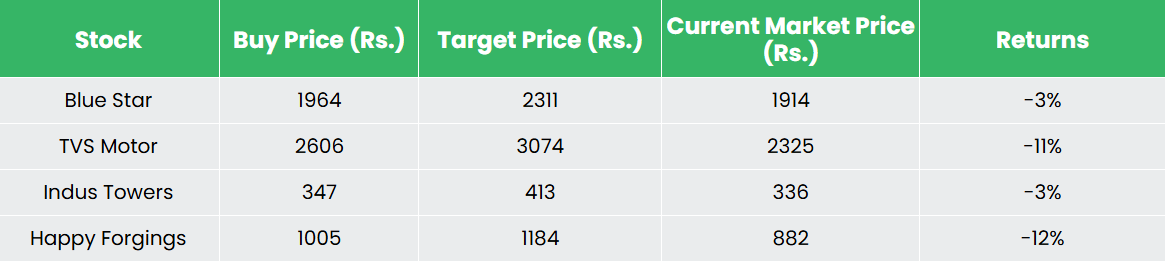

Recap of our previous recommendations (As on 21 February 2025)

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.

Other articles you may like

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}