On August 27, 2020, the US Federal Reserve Chairman, Jerome Powell made a path breaking speech – New Economic Challenges and the Fed’s Monetary Policy Review. On the same day, the Federal Reserve Bank released a statement – Federal Open Market Committee announces approval of updates to its Statement on Longer-Run Goals and Monetary Policy Strategy. I analysed that shift in this blog post – US Federal Reserve statement signals a new phase in the paradigm shift in macroeconomics (August 31, 2020). It appeared at the time, that a major shift in the way central banking policy was to be conducted in the future was underway. A Reuters’ report (August 28, 2020) – With new monetary policy approach, Fed lays Phillips curve to rest – reported that “One of the fundamental theories of modern economics may have finally been put to rest”. At the time, I didn’t place enough emphasis on the ‘may’ and now realise that nothing really has changed after a few years of teetering on the precipice of change. The old guard is back and threatening the livelihoods of workers in their usual way.

Powell’s August 2020 shift meant that the central bank was to focus on creating “maximum employment” rather than sacrifice jobs growth because some measure of future expected inflation had risen above the desired rate.

It meant that the central bank would no longer tighten monetary policy as employment growth strengthens before there are inflationary effects – that is, they are rejecting all the ‘forward-looking’ bias that mainstream theory imparted that policy had to kill off employment growth before unemployment had fallen significantly.

After Powell’s apparent shift several other central banks followed suit with similar commitments to full employment and a more calm attitude to inflation dynamics.

And, unemployment fell all around the world, which is a good thing for workers.

Someone must have been reading Robert Louis Stevenson, because within the space of a few months Mr Hyde is back in town, more lethal than before.

The ECB has just run a conference in Sintra (Portugal) and Jerome Powell appeared yesterday (June 29, 2022) with ECB boss Madame Lagarde and basically confirmed that our hopes that a real change had occurred in 2020 were just a pipe dream.

Powell’s narrative took us back to the 1980s and onwards with talk about ‘soft landings’ and an ‘inflation first’ imperative.

He claimed that the Federal Reserve was no prioritising its fight against inflation and would be raising interest rates “just enough” to achieve that goal.

The problem is that central bankers do not know what ‘just enough’ is because of the inexact nature of monetary policy exercised through interest rate increases.

We have always known it to be a rather ‘blunt’ policy tool – which just means there are several reasons why impacts are ambiguous and subject to unpredictable time lags.

First, central bankers do not know whether interest rate increases take pressure of price rises. There is every reason, at least in the short-run to expect they worsen the inflationary pressures, especially if those pressures are the result of corporations exercising market power to pass on rising unit costs via their mark-ups.

Second, there are also counter distributional effects of interest rate rises, where creditors and those on fixed incomes enjoy a stimulus and debtors endure reduced purchasing power.

How those distributional impacts play out is uncertain.

Third, there are time lags that are unpredictable. Even under mainstream logic, the rate rises influence interest-rate sensitive costs and expenditures. They are not linear in impact.

People take time to adjust and may well, for example, just eat into prior savings before curtailing expenditure and borrowing.

Time lags make policy difficult to implement because if the aim is to influence the cycle and the policy intervention only starts to impact when the cycle has already shifted then the outcomes can be perverse indeed.

Fourth, eventually, interest rate levels will reach such a height that they cause recession and an escalation in unemployment, which discourages the firms from exercising that market power as costs drive bankruptcies and even OPEC oil sellers realise they are losing profits due to volume falls.

But the economic and social cost of that strategy is massive and unjustifiable.

At least according to my calculus.

But not, it seems to the likes of Powell.

He told the audience at Sintra:

Is there a risk that we would go too far? Certainly there’s a risk, but I wouldn’t agree that it’s the biggest risk to the economy … The bigger mistake to make, let’s put it that way, would be to fail to restore price stability.

He also said that there was “no guarantee” that the Federal Reserve would not create a recession as a result of the current policy shift.

So unemployment is not the biggest risk – which is the familiar narrative in the neoliberal era.

Deliberately creating recession – the worst of economic evils – is now back within the policy set – a sort of contagion outcome.

Unemployment is no longer a policy target to be kept low, but a deliberate policy tool to be used to keep inflation low.

Every time I have done the calculations on the relative costs and benefits of that strategy the answer is the same – costs massive, benefits low.

It can never be a responsible and efficient strategy to waste millions of income generating potential on a daily basis just to see inflation drop to low levels.

Powell also admitted that the inflationary pressures were coming from the on-going effects on the pandemic and more recently, the Russian invasion of Ukraine.

He didn’t mention the anti-competitive behaviour of OPEC who exert monopoly power to push up oil prices to suit their own ends.

But the point is that if it is true that these factors are driving the inflationary pressures, then how does raising interest rates solve the problems that those factors present?

By increasing the borrowing costs they might be able to influence demand, but will do nothing to influence the shipping disruptions, factory closures, increasing pools of sick workers from Covid, the Russian invasion, and OPEC.

There is no answer from the central bankers to this anomaly other than to return to script.

1. Inflation must be our priority.

2. Inflationary expectations might escape and become self-fulfilling.

3. The only tool we have is to drive the economy into recession, induce rising poverty, etc.

4. But we won’t comment on the obscene CEO salary increases that get reported each day in the financial press.

Back to the 1980s.

It is a complete contradiction of the August 2020 statement.

We are now back to the ‘forward-looking’ approach – where even before any expectational blowouts have been detected – the central bank hikes rates and drives unemployment up.

It is a very costly strategy.

What they are effectively saying is that even though there are supply constraints, they are prepared to reduce aggregate demand down to the reduced level of supply.

The question then is what happens when supply recovers as factories reopen, ships move around and so on?

Well then they will be left with a massive pool of jobless people, some of whom will have been forced to default on their mortgages and lose their houses as a consequence, some of whom will have committed suicide, not to mention the generation of workers leaving school who will face limited opportunities in the labour market to progress with.

A clusterf*xk!

It would be far better to understand that the inflationary pressures are transitory and to maintain low levels of unemployment while the transitory factors play out.

Powell and Lagarde told the Sintra conference that they had waited to raise interest rates because they through the rising prices were the “temporary result of supply chain” disruptions due to Covid.

And indeed they are.

The mistake they are making is to equate “temporary” with short-term.

Transitory does not have a time element. It has a causal element.

The causes will take time to work out that is beyond doubt.

But it is folly to add an additional (very costly) problem into the mix (recession) when those causal factors will dissipate eventually.

The other claim these central bankers made at Sintra was that there are plenty of private savings in the system which will act as a buffer against the rising interest rates.

In other words, deliberately create unemployment and income loss, and hope that expenditure doesn’t fall as much as the unemployed are forced to run down their wealth holdings to stay afloat.

All of which will devastate lower income households.

The only central bank that is holding firm at present against all this madness is the Bank of Japan. Smart.

The European Commission Spring Forecasts

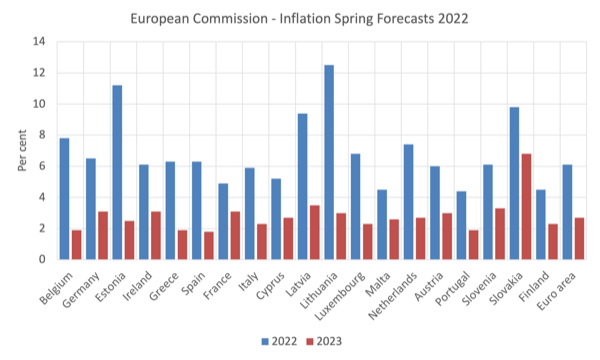

If you go back and read the European Commission’s – Spring 2022 Economic Forecast: Russian invasion tests EU economic resilience – you will note that the inflation forecasts for 2022 and 2023 do not signify any entrenched inflation problem.

The following graph shows the forecasts for 2022 and 2023.

Spot any major on-going inflationary acceleration.

Now the Commission may be wrong (probable) but the way the ECB is now talking – lockstep with the irresponsible US Federal Reserve – one can clearly see a breakdown in policy coherence in Europe at least.

The Commission think inflation will dissipate quickly by next year – while the ECB is talking about being prepared to create a recession to ‘tame’ accelerating inflation.

Conclusion

Unaccountable central bankers once again out of control.

That is enough for today!

(c) Copyright 2022 William Mitchell. All Rights Reserved.

{kind=link}